%22%20fill%3D%22%23021A43%22%3E%3Cpath%20d%3D%22M267.109551%2C33.9224%20L301.032051%2C0%20L334.954551%2C33.9224%20L329.125351%2C39.7516%20L301.032051%2C11.6583%20L272.938751%2C39.7516%20L267.109551%2C33.9224%20Z%20M322.483751%2C64.3549%20L338.106051%2C79.9772%20L332.276951%2C85.8064%20L316.654651%2C70.1841%20L301.032051%2C85.8064%20L267.109551%2C51.8839%20L272.938751%2C46.055%20L301.032051%2C74.1483%20L329.125351%2C46.055%20L334.954551%2C51.8839%20L322.483751%2C64.3549%20Z%22%20id%3D%22Fill-3%22%3E%3C%2Fpath%3E%3Cg%20id%3D%22v%22%20transform%3D%22translate(0%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpolygon%20id%3D%22Path%22%20points%3D%2223.1661333%200%2029.9750083%200%2018.1392686%2027.7674434%2011.8357397%2027.7674434%200%200%206.99505518%200%2015.0539971%2020.2404448%22%3E%3C%2Fpolygon%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(30.6833%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(65.3066%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(86.731%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22b%22%20transform%3D%22translate(123.2691%2C%2021.9462)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M15.9051064%2C10.7984502%20C18.4584346%2C10.7984502%2020.7812539%2C11.4323494%2022.8735645%2C12.7001477%20C24.965875%2C13.967946%2026.6060337%2C15.7144934%2027.7940405%2C17.9397898%20C28.9820474%2C20.1650862%2029.5760508%2C22.6341899%2029.5760508%2C25.3471011%20C29.5760508%2C28.0600122%2028.9820474%2C30.529116%2027.7940405%2C32.7544124%20C26.6060337%2C34.9797087%2024.965875%2C36.7262561%2022.8735645%2C37.9940544%20C20.7812539%2C39.2618528%2018.4584346%2C39.895752%2015.9051064%2C39.895752%20C13.8837217%2C39.895752%2012.0396514%2C39.4879287%2010.3728955%2C38.6722822%20C8.70613965%2C37.8566357%207.28762402%2C36.6952261%206.11734863%2C35.1880532%20L6.11734863%2C39.2308228%20L-5.68434189e-14%2C39.2308228%20L-5.68434189e-14%2C0%20L6.11734863%2C0%20L6.11734863%2C15.4795518%20C7.26989258%2C13.9901104%208.68397534%2C12.8375664%2010.3595969%2C12.0219199%20C12.0352185%2C11.2062734%2013.8837217%2C10.7984502%2015.9051064%2C10.7984502%20Z%20M8.56428809%2C31.517644%20C10.2133125%2C33.1666685%2012.2612944%2C33.9911807%2014.7082339%2C33.9911807%20C17.1551733%2C33.9911807%2019.1942896%2C33.1622356%2020.8255825%2C31.5043455%20C22.4568755%2C29.8464553%2023.272522%2C27.7940405%2023.272522%2C25.3471011%20C23.272522%2C22.9001616%2022.4568755%2C20.843314%2020.8255825%2C19.1765581%20C19.1942896%2C17.5098022%2017.1551733%2C16.6764243%2014.7082339%2C16.6764243%20C12.2612944%2C16.6764243%2010.2177454%2C17.5098022%208.57758667%2C19.1765581%20C6.93742798%2C20.843314%206.11734863%2C22.9001616%206.11734863%2C25.3471011%20C6.11734863%2C27.7940405%206.93299512%2C29.8508882%208.56428809%2C31.517644%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22o%22%20transform%3D%22translate(156.5624%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M14.8678169%2C29.0973018%20C10.6300015%2C29.0973018%207.09257812%2C27.7053833%204.25554687%2C24.9215464%20C1.41851562%2C22.1377095%200%2C18.6800776%200%2C14.5486509%20C0%2C10.4172241%201.41851562%2C6.95959229%204.25554687%2C4.17575537%20C7.09257812%2C1.39191846%2010.6300015%2C0%2014.8678169%2C0%20C17.6339224%2C0%2020.1562205%2C0.63389917%2022.4347112%2C1.90169751%20C24.7132019%2C3.16949585%2026.499645%2C4.91604321%2027.7940405%2C7.1413396%20C29.088436%2C9.36663599%2029.7356338%2C11.8357397%2029.7356338%2C14.5486509%20C29.7356338%2C17.261562%2029.088436%2C19.7306658%2027.7940405%2C21.9559622%20C26.499645%2C24.1812585%2024.7132019%2C25.9278059%2022.4347112%2C27.1956042%20C20.1562205%2C28.4634026%2017.6339224%2C29.0973018%2014.8678169%2C29.0973018%20Z%20M8.72387109%2C20.7191938%20C10.3728955%2C22.3682183%2012.4208774%2C23.1927305%2014.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.4208774%2C5.87797412%2010.3728955%2C6.71135205%208.72387109%2C8.37810791%20C7.07484668%2C10.0448638%206.25033447%2C12.1017114%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07484668%2C19.052438%208.72387109%2C20.7191938%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22u%22%20transform%3D%22translate(191.1474%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M12.8464321%2C28.4323726%20C8.98097705%2C28.4323726%205.87354126%2C27.3596201%203.52412476%2C25.2141152%20C1.17470825%2C23.0686104%200%2C20.2315791%200%2C16.7030215%20L0%2C0%20L6.09075146%2C0%20L6.09075146%2C15.9051064%20C6.09075146%2C17.8910283%206.71135205%2C19.4912913%207.95255322%2C20.7058953%20C9.19375439%2C21.9204993%2010.8250474%2C22.5278013%2012.8464321%2C22.5278013%20C14.8678169%2C22.5278013%2016.4902441%2C21.9249321%2017.7137139%2C20.7191938%20C18.9371836%2C19.5134556%2019.5489185%2C17.9087598%2019.5489185%2C15.9051064%20L19.5489185%2C0%20L25.6396699%2C0%20L25.6396699%2C16.7030215%20C25.6396699%2C20.2315791%2024.4693945%2C23.0686104%2022.1288437%2C25.2141152%20C19.788293%2C27.3596201%2016.6941558%2C28.4323726%2012.8464321%2C28.4323726%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(221.2498%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fsvg%3E)

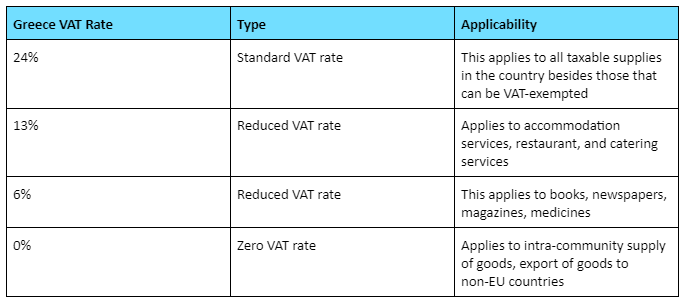

VAT in Greece - Three Types of Rates

There are three types of VAT rates in Greece:

- Standard VAT rate,

- Reduced VAT rates,

- Zero VAT rate.

How much is VAT in Greece's Regions?

The Greek Ministry of Economy and Finance reduced all applicable rates by 30% on the Aegean islands of Leros, Lesvos, Kos, Samos, and Chios. Therefore, the standard VAT rate is 17%, and reduced VAT rates are 9% and 4%.

These rates apply to goods located on these islands and sold by the taxable persons established on one of the islands or sold by the taxable person not based on these islands. Still, the goods are to be delivered to these islands to the buyer that is established or located on these islands.

Regarding the provision of services, these special VAT rates apply when both of the following requirements are met:

- Services are provided by the taxpayer established on these islands, meaning that it has a registered seat, headquarters, or branch that provides these services permanently and

- Services are provided within these islands.

VAT Registration Threshold

The VAT legislation contains relevant information about the VAT threshold in Greece and its applicable provisions. Interpreting the appropriate information shared by Tax Authority officials is also a helpful source of information.

There is no VAT threshold in Greece for resident or non-resident businesses. This means that all businesses with a registered office or a permanent establishment in Greece that carry out taxable activities, tax-exempt activities for which they have the right to deduct input tax, or taxable activities outside Greece with a right to deduct should register for VAT purposes regardless of the annual income.

In other words, resident and non-resident businesses should register for VAT if they perform taxable activities.

Similarly, there is no registration threshold for non-EU established suppliers of Electronically Supplied Services.

Greece implemented an EU-wide VAT registration threshold of EUR 10,000 for intra-EU distance sales of goods and B2C supplies of services.

Types of Taxable Activities in Greece

Under the Greece VAT Law, any natural or legal person, either resident or foreign, can be considered a taxable person if they carry out independent economic activity, regardless of the purpose and results of such activity.

Activities that are considered as economic or taxable activities are:

- The supply of goods and provision of services in Greece for a fee;

- Reverse-charge services received by a taxable person in Greece;

- Export and import of goods;

VAT Registration Process

Since there is no VAT registration threshold, all businesses that carry out taxable activities should register with the Tax Authority. During that process, they receive a tax registration number that they use for all tax-related issues, including VAT.

Greece VAT Registration for Domestic Businesses

The VAT registration process, required documents, and tax forms for domestic businesses depend on their legal form and registered address.

The time needed to receive a VAT number is usually one week from when all the necessary documents are submitted.

Greece VAT Registration for Foreign Businesses

The VAT registration process for foreign businesses in Greece depends on whether the businesses are established in an EU Member State or a non-EU country.

EU-based businesses can register directly for VAT purposes in Greece through e-mail correspondence with the competent Tax Office in Athens. After receiving the registration form, the Tax Office verifies all the data, registers the businesses in the TAXIS system, and issues a VAT registration number. Once this procedure is completed, EU-based businesses receive all the information through an email.

In contrast, non-EU businesses should appoint a fiscal representative to complete the VAT registration process. The fiscal representative should submit documents such as a Power of Attorney and Memorandum of Association translated into Greek to the Tax Authority with the registration form.

VAT Returns in Greece

Whether domestic or foreign, businesses registered or VAT in Greece should submit monthly or quarterly VAT returns through the government TAXISnet system. In some cases, semiannual or half-annual returns are required.

Public sector organizations and businesses using double-entry bookkeeping should submit monthly VAT returns, while businesses using single-entry bookkeeping and those exempt from the bookkeeping obligations should submit quarterly returns.

Businesses using a flat-rate scheme should submit a hard copy of the VAT return every six months. When businesses carry out activities related to a flat-rate scheme and another taxable activity, a semiannual VAT return and VAT return relating to other activities are required.

The deadline for filing the VAT return is the last day of the month following the reporting period, regardless of the type of VAT return.

Penalties for Failure to File Tax Return

Non-compliance with VAT Greece registration rules and the deadline for submitting VAT returns can result in finance penalties and interest.

When inaccurate VAT returns are submitted, resulting in non-payment, partial payment, or refund of VAT, and the Tax Authority notices this during an audit, businesses may be penalized up to 50% of the due VAT. The same penalty applies in the case of non-submission of a VAT return.

Late submissions of VAT returns result in procedural penalties of EUR 102,40 and 500, depending on the types of bookkeeping rules that apply to the businesses.

Submitting a late amending VAT return will not result in a procedural penalty if the initial VAT return was submitted on time. However, interest may be calculated for late payments.

If a business fails to register on time for VAT but eventually registers voluntarily, the penalty is EUR 102,40. On the other hand, if it completely fails to register for VAT purposes, the penalty is EUR 2,500.

VAT Rules for Electronically Supplied Services

Under the EU VAT Directive 2006/112/EC, only services delivered automatically, with little to no human intervention, through the use of the Internet can be considered Electronically Supplied Services (ESS)

As an EU Member State, Greece, just like other EU countries, adopted the standard definition of the ESS in its national legislation.

Taxability Rules for ESS:

An EU-wide rule governs the B2B supply of ESS, meaning that the place of supply is where the client is established. Similarly, non-EU businesses should comply with EU rules relating to the B2C supply of ESS and calculate VAT in the country where the consumer resides.

The EUR 10,000 threshold is crucial in determining the VAT rules for distance sales of goods and B2C ESS. Businesses that exceed this threshold apply VAT rates in the country where the customer is located. In contrast, businesses that remain under the threshold can apply VAT rates of their country or voluntarily register for One-Stop Shop (OSS) schemes.

How much is VAT in Greece on ESS?

The Greece VAT rate for ESS is 24%.

E-Commerce Rules

E-commerce rules have changed a lot in past years, and the changes in 2021 are the most significant ones since they introduced a new EU-wide EUR 10,000 threshold and enlarged Mini OSS, now known as OSS. These changes to Mini OSS brought the Import One Stop Shop (IOSS) for B2C sales of imported goods from third countries of up to EUR 150.

Furthermore, deemed supplier rules were introduced for digital platforms, as they became persons liable for VAT purposes.

From 2021, the OSS system has three schemes:

- Union Scheme,

- Non-Union Scheme,

- Import Scheme.

VAT EU Reporting

In Greece, businesses should submit both the EC Sales List and Intrastat.

EC Sales List

Both domestic and foreign businesses registered for VAT Greece should submit monthly EC Sales Lists (ESL) electronically. Transactions such as Intra-community supply and acquisitions of goods and services subject to reverse charge should be included in ECL reports.

The ECL is submitted when the stated transaction happens, while nil ESL is not required if there are no such transactions.

The deadline for submission of ESL is the 26th of the month following the reporting period, and businesses not complying with this rule risk a penalty of EUR 100.

Intrastat

Businesses that should submit Intrastat reports are those whose intra-EU imports exceed the EUR 150,000 threshold or whose intra-EU exports are EUR 90,000. The Intrastat is submitted electronically through the Hellenic Statistical Authority (EL.STAT).

Digital Reporting

Local Businesses

Local businesses in Greece should issue e-invoices only for B2G transactions through the national platform MyData. Until mandatory rules are introduced, businesses can voluntarily issue B2B transactions using the MyData service.

%22%20fill%3D%22%23FFFFFF%22%3E%3Cpath%20d%3D%22M267.109551%2C33.9224%20L301.032051%2C0%20L334.954551%2C33.9224%20L329.125351%2C39.7516%20L301.032051%2C11.6583%20L272.938751%2C39.7516%20L267.109551%2C33.9224%20Z%20M322.483751%2C64.3549%20L338.106051%2C79.9772%20L332.276951%2C85.8064%20L316.654651%2C70.1841%20L301.032051%2C85.8064%20L267.109551%2C51.8839%20L272.938751%2C46.055%20L301.032051%2C74.1483%20L329.125351%2C46.055%20L334.954551%2C51.8839%20L322.483751%2C64.3549%20Z%22%20id%3D%22Fill-3%22%3E%3C%2Fpath%3E%3Cg%20id%3D%22v%22%20transform%3D%22translate(0%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpolygon%20id%3D%22Path%22%20points%3D%2223.1661333%200%2029.9750083%200%2018.1392686%2027.7674434%2011.8357397%2027.7674434%200%200%206.99505518%200%2015.0539971%2020.2404448%22%3E%3C%2Fpolygon%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(30.6833%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(65.3066%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(86.731%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22b%22%20transform%3D%22translate(123.2691%2C%2021.9462)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M15.9051064%2C10.7984502%20C18.4584346%2C10.7984502%2020.7812539%2C11.4323494%2022.8735645%2C12.7001477%20C24.965875%2C13.967946%2026.6060337%2C15.7144934%2027.7940405%2C17.9397898%20C28.9820474%2C20.1650862%2029.5760508%2C22.6341899%2029.5760508%2C25.3471011%20C29.5760508%2C28.0600122%2028.9820474%2C30.529116%2027.7940405%2C32.7544124%20C26.6060337%2C34.9797087%2024.965875%2C36.7262561%2022.8735645%2C37.9940544%20C20.7812539%2C39.2618528%2018.4584346%2C39.895752%2015.9051064%2C39.895752%20C13.8837217%2C39.895752%2012.0396514%2C39.4879287%2010.3728955%2C38.6722822%20C8.70613965%2C37.8566357%207.28762402%2C36.6952261%206.11734863%2C35.1880532%20L6.11734863%2C39.2308228%20L-5.68434189e-14%2C39.2308228%20L-5.68434189e-14%2C0%20L6.11734863%2C0%20L6.11734863%2C15.4795518%20C7.26989258%2C13.9901104%208.68397534%2C12.8375664%2010.3595969%2C12.0219199%20C12.0352185%2C11.2062734%2013.8837217%2C10.7984502%2015.9051064%2C10.7984502%20Z%20M8.56428809%2C31.517644%20C10.2133125%2C33.1666685%2012.2612944%2C33.9911807%2014.7082339%2C33.9911807%20C17.1551733%2C33.9911807%2019.1942896%2C33.1622356%2020.8255825%2C31.5043455%20C22.4568755%2C29.8464553%2023.272522%2C27.7940405%2023.272522%2C25.3471011%20C23.272522%2C22.9001616%2022.4568755%2C20.843314%2020.8255825%2C19.1765581%20C19.1942896%2C17.5098022%2017.1551733%2C16.6764243%2014.7082339%2C16.6764243%20C12.2612944%2C16.6764243%2010.2177454%2C17.5098022%208.57758667%2C19.1765581%20C6.93742798%2C20.843314%206.11734863%2C22.9001616%206.11734863%2C25.3471011%20C6.11734863%2C27.7940405%206.93299512%2C29.8508882%208.56428809%2C31.517644%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22o%22%20transform%3D%22translate(156.5624%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M14.8678169%2C29.0973018%20C10.6300015%2C29.0973018%207.09257812%2C27.7053833%204.25554687%2C24.9215464%20C1.41851562%2C22.1377095%200%2C18.6800776%200%2C14.5486509%20C0%2C10.4172241%201.41851562%2C6.95959229%204.25554687%2C4.17575537%20C7.09257812%2C1.39191846%2010.6300015%2C0%2014.8678169%2C0%20C17.6339224%2C0%2020.1562205%2C0.63389917%2022.4347112%2C1.90169751%20C24.7132019%2C3.16949585%2026.499645%2C4.91604321%2027.7940405%2C7.1413396%20C29.088436%2C9.36663599%2029.7356338%2C11.8357397%2029.7356338%2C14.5486509%20C29.7356338%2C17.261562%2029.088436%2C19.7306658%2027.7940405%2C21.9559622%20C26.499645%2C24.1812585%2024.7132019%2C25.9278059%2022.4347112%2C27.1956042%20C20.1562205%2C28.4634026%2017.6339224%2C29.0973018%2014.8678169%2C29.0973018%20Z%20M8.72387109%2C20.7191938%20C10.3728955%2C22.3682183%2012.4208774%2C23.1927305%2014.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.4208774%2C5.87797412%2010.3728955%2C6.71135205%208.72387109%2C8.37810791%20C7.07484668%2C10.0448638%206.25033447%2C12.1017114%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07484668%2C19.052438%208.72387109%2C20.7191938%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22u%22%20transform%3D%22translate(191.1474%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M12.8464321%2C28.4323726%20C8.98097705%2C28.4323726%205.87354126%2C27.3596201%203.52412476%2C25.2141152%20C1.17470825%2C23.0686104%200%2C20.2315791%200%2C16.7030215%20L0%2C0%20L6.09075146%2C0%20L6.09075146%2C15.9051064%20C6.09075146%2C17.8910283%206.71135205%2C19.4912913%207.95255322%2C20.7058953%20C9.19375439%2C21.9204993%2010.8250474%2C22.5278013%2012.8464321%2C22.5278013%20C14.8678169%2C22.5278013%2016.4902441%2C21.9249321%2017.7137139%2C20.7191938%20C18.9371836%2C19.5134556%2019.5489185%2C17.9087598%2019.5489185%2C15.9051064%20L19.5489185%2C0%20L25.6396699%2C0%20L25.6396699%2C16.7030215%20C25.6396699%2C20.2315791%2024.4693945%2C23.0686104%2022.1288437%2C25.2141152%20C19.788293%2C27.3596201%2016.6941558%2C28.4323726%2012.8464321%2C28.4323726%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(221.2498%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fsvg%3E)