%22%20fill%3D%22%23021A43%22%3E%3Cpath%20d%3D%22M267.109551%2C33.9224%20L301.032051%2C0%20L334.954551%2C33.9224%20L329.125351%2C39.7516%20L301.032051%2C11.6583%20L272.938751%2C39.7516%20L267.109551%2C33.9224%20Z%20M322.483751%2C64.3549%20L338.106051%2C79.9772%20L332.276951%2C85.8064%20L316.654651%2C70.1841%20L301.032051%2C85.8064%20L267.109551%2C51.8839%20L272.938751%2C46.055%20L301.032051%2C74.1483%20L329.125351%2C46.055%20L334.954551%2C51.8839%20L322.483751%2C64.3549%20Z%22%20id%3D%22Fill-3%22%3E%3C%2Fpath%3E%3Cg%20id%3D%22v%22%20transform%3D%22translate(0%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpolygon%20id%3D%22Path%22%20points%3D%2223.1661333%200%2029.9750083%200%2018.1392686%2027.7674434%2011.8357397%2027.7674434%200%200%206.99505518%200%2015.0539971%2020.2404448%22%3E%3C%2Fpolygon%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(30.6833%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(65.3066%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(86.731%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22b%22%20transform%3D%22translate(123.2691%2C%2021.9462)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M15.9051064%2C10.7984502%20C18.4584346%2C10.7984502%2020.7812539%2C11.4323494%2022.8735645%2C12.7001477%20C24.965875%2C13.967946%2026.6060337%2C15.7144934%2027.7940405%2C17.9397898%20C28.9820474%2C20.1650862%2029.5760508%2C22.6341899%2029.5760508%2C25.3471011%20C29.5760508%2C28.0600122%2028.9820474%2C30.529116%2027.7940405%2C32.7544124%20C26.6060337%2C34.9797087%2024.965875%2C36.7262561%2022.8735645%2C37.9940544%20C20.7812539%2C39.2618528%2018.4584346%2C39.895752%2015.9051064%2C39.895752%20C13.8837217%2C39.895752%2012.0396514%2C39.4879287%2010.3728955%2C38.6722822%20C8.70613965%2C37.8566357%207.28762402%2C36.6952261%206.11734863%2C35.1880532%20L6.11734863%2C39.2308228%20L-5.68434189e-14%2C39.2308228%20L-5.68434189e-14%2C0%20L6.11734863%2C0%20L6.11734863%2C15.4795518%20C7.26989258%2C13.9901104%208.68397534%2C12.8375664%2010.3595969%2C12.0219199%20C12.0352185%2C11.2062734%2013.8837217%2C10.7984502%2015.9051064%2C10.7984502%20Z%20M8.56428809%2C31.517644%20C10.2133125%2C33.1666685%2012.2612944%2C33.9911807%2014.7082339%2C33.9911807%20C17.1551733%2C33.9911807%2019.1942896%2C33.1622356%2020.8255825%2C31.5043455%20C22.4568755%2C29.8464553%2023.272522%2C27.7940405%2023.272522%2C25.3471011%20C23.272522%2C22.9001616%2022.4568755%2C20.843314%2020.8255825%2C19.1765581%20C19.1942896%2C17.5098022%2017.1551733%2C16.6764243%2014.7082339%2C16.6764243%20C12.2612944%2C16.6764243%2010.2177454%2C17.5098022%208.57758667%2C19.1765581%20C6.93742798%2C20.843314%206.11734863%2C22.9001616%206.11734863%2C25.3471011%20C6.11734863%2C27.7940405%206.93299512%2C29.8508882%208.56428809%2C31.517644%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22o%22%20transform%3D%22translate(156.5624%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M14.8678169%2C29.0973018%20C10.6300015%2C29.0973018%207.09257812%2C27.7053833%204.25554687%2C24.9215464%20C1.41851562%2C22.1377095%200%2C18.6800776%200%2C14.5486509%20C0%2C10.4172241%201.41851562%2C6.95959229%204.25554687%2C4.17575537%20C7.09257812%2C1.39191846%2010.6300015%2C0%2014.8678169%2C0%20C17.6339224%2C0%2020.1562205%2C0.63389917%2022.4347112%2C1.90169751%20C24.7132019%2C3.16949585%2026.499645%2C4.91604321%2027.7940405%2C7.1413396%20C29.088436%2C9.36663599%2029.7356338%2C11.8357397%2029.7356338%2C14.5486509%20C29.7356338%2C17.261562%2029.088436%2C19.7306658%2027.7940405%2C21.9559622%20C26.499645%2C24.1812585%2024.7132019%2C25.9278059%2022.4347112%2C27.1956042%20C20.1562205%2C28.4634026%2017.6339224%2C29.0973018%2014.8678169%2C29.0973018%20Z%20M8.72387109%2C20.7191938%20C10.3728955%2C22.3682183%2012.4208774%2C23.1927305%2014.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.4208774%2C5.87797412%2010.3728955%2C6.71135205%208.72387109%2C8.37810791%20C7.07484668%2C10.0448638%206.25033447%2C12.1017114%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07484668%2C19.052438%208.72387109%2C20.7191938%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22u%22%20transform%3D%22translate(191.1474%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M12.8464321%2C28.4323726%20C8.98097705%2C28.4323726%205.87354126%2C27.3596201%203.52412476%2C25.2141152%20C1.17470825%2C23.0686104%200%2C20.2315791%200%2C16.7030215%20L0%2C0%20L6.09075146%2C0%20L6.09075146%2C15.9051064%20C6.09075146%2C17.8910283%206.71135205%2C19.4912913%207.95255322%2C20.7058953%20C9.19375439%2C21.9204993%2010.8250474%2C22.5278013%2012.8464321%2C22.5278013%20C14.8678169%2C22.5278013%2016.4902441%2C21.9249321%2017.7137139%2C20.7191938%20C18.9371836%2C19.5134556%2019.5489185%2C17.9087598%2019.5489185%2C15.9051064%20L19.5489185%2C0%20L25.6396699%2C0%20L25.6396699%2C16.7030215%20C25.6396699%2C20.2315791%2024.4693945%2C23.0686104%2022.1288437%2C25.2141152%20C19.788293%2C27.3596201%2016.6941558%2C28.4323726%2012.8464321%2C28.4323726%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(221.2498%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fsvg%3E)

When discussing digital trade and e-commerce, Cambodia is not one of the Asian countries that first comes to mind. Even though the country is steadily growing, its economy still lags behind several of its Southeast Asian neighbors, including Thailand, Vietnam, and Indonesia, which have more diversified industries and higher levels of economic output. Nonetheless, where Cambodia is not behind other Asian countries is in implementing VAT e-commerce rules for foreign suppliers.

Cambodia’s VAT Framework for E-commerce

Following the footsteps of the Philippines, Singapore, Indonesia, and Malaysia, which were the early adopters of VAT on e-commerce and digital services in Asia, Cambodia issued Sub-Decree No. 65 on the Implementation of VAT on E-commerce in 2022, along with Prakas 542.

Together, these two documents set the formal legal framework and provide detailed guidance on how the rules apply to non-resident suppliers. As a result, since April 1, 2022, foreign businesses that provide e-commerce services to Cambodian customers may be subject to VAT obligations.

It is vital to note that e-commerce is broadly defined as commercial activities conducted through electronic systems, including the purchase, sale, rental, or exchange of goods or services via digital platforms or online technologies. The definition is intentionally broad, encompassing both business and civil transactions conducted electronically, reflecting the growing role of digital platforms in facilitating economic activity.

Consequently, the supply of digital goods and services falls under this broad definition of e-commerce. Digital goods are considered intangible products ordered, supplied, and delivered through electronic systems, such as downloadable software, digital media, or online content. Digital services, on the other hand, include a wide range of services supplied electronically, such as cloud computing, online advertising, application hosting, and streaming services.

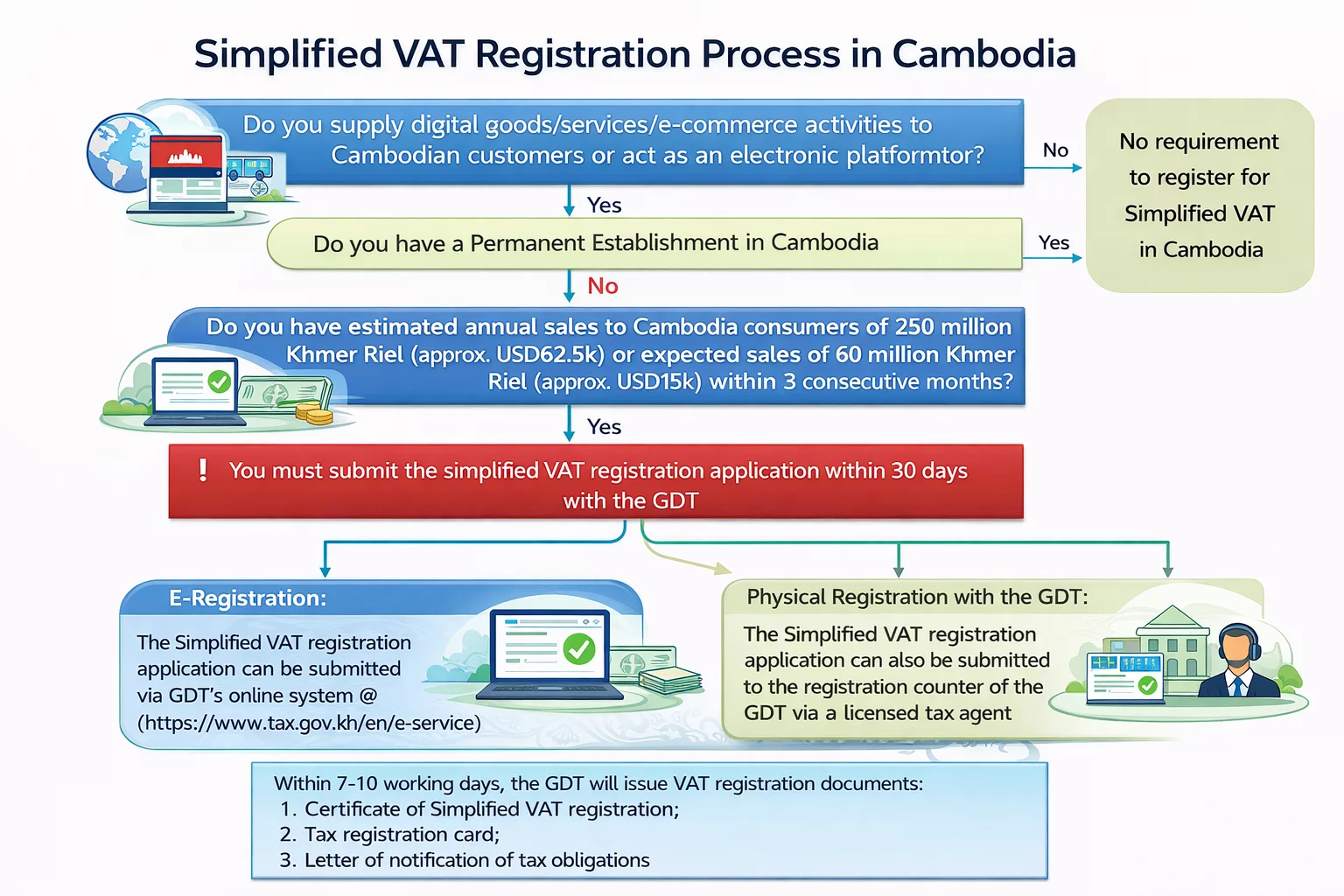

Foreign Businesses Affected by E-commerce Regulations

The Cambodian VAT rules apply primarily to non-resident or foreign taxable persons who supply digital goods, digital services, or other e-commerce activities to customers located in Cambodia. These are the businesses that are not physically present or do not have a permanent establishment in the country but generate revenue from Cambodian users through online platforms or digital delivery.

Examples of affected businesses may include streaming platforms, software-as-a-service (SaaS) providers, online advertising companies, cloud computing providers, and operators of online marketplaces that facilitate digital transactions. More specifically, companies such as Meta, Microsoft, Google, Zoom, Amazon, Netflix, Booking.com, all fall under the scope of these rules.

However, providing e-commerce services is not the only relevant factor to becoming liable for VAT in Cambodia. Only foreign businesses with an annual turnover from KHR 250 million (approximately USD 62,500) or a total expected turnover for three consecutive months ending in the current calendar year of KHR 60 million (approximately USD 15,000) are required to register for VAT.

Once either of these two thresholds is exceeded, foreign digital and e-commerce companies must complete a simplified VAT registration process with Cambodia’s General Department of Taxation (GDT) within 30 days. The registration is completed by filing a VAT application form, along with several mandatory supporting documents, including proof of tax registration in their home country, valid identification for the owner or authorized representative, and confirmation of a bank account issued or printed by the taxable person’s bank.

Note: Data in the image is from the International Monetary Fund - Introducing Cambodia’s VAT on E-Commerce

Reporting and Other Requirements for Foreign E-commerce Suppliers

After foreign businesses complete the VAT registration process, these suppliers must comply with ongoing reporting and tax payment obligations. First of all, foreign suppliers must charge a 10% VAT on sales to residents who are not registered under the self-declaration regime, B2C transactions, and must submit monthly VAT returns to the GDT.

In contrast, for B2B transactions, the reverse-charge mechanism applies, with a notable exception. Small domestic taxable persons are exempt from this reverse-charge requirement for a period of five years, effective September 8, 2021. This means that non-resident suppliers providing services to these customers must collect and remit the 10% VAT directly to the GDT.

Importantly, foreign businesses supplying digital goods, digital services, or any e-commerce activity to local customers must issue an invoice with specific information depending on the customer's type. For B2C transactions, the invoice must include the company name, the Simplified VAT Registration identification number, the invoice number, the date of issuance, the customer’s address in Cambodia and email, a description of the goods or services provided, the unit, the unit price, and the total price.

For B2C transactions, the invoice must include the supplier’s name and Tax Identification Number, the invoice number, the date of issuance, the name and Tax Identification Number of the customer, the customer’s address in Cambodia and email, a description of the goods or services, the unit, the unit price, and the total price.

Key Compliance Tips for Foreign Businesses

Foreign e-commerce suppliers entering the Cambodian market must carefully assess whether their digital activities fall under the scope of the country's VAT rules, especially since some of these activities are broadly defined.

Additionally, the GDT retained the authority to register e-commerce suppliers that fail to register voluntarily after being invited to do so. The GDT may obtain information about potentially taxable activities from multiple sources, including reverse-charge reports submitted by local businesses and withholding tax information filed through electronic systems. Thus, businesses providing digital services to Cambodian customers should carefully assess their compliance obligations to avoid potential risks associated with non-registration or non-compliance.

Furthemore, businesses registered for VAT in Cambodia that collect and remit VAT on B2B transactions with small domestic taxable persons must be aware that the five-year exemption period will end this September. From that point on, if no changes are made, they will no longer be liable for this VAT, and continuing collection and remittance will impose unnecessary financial and administrative burdens.

Source: Cambodian General Department of Taxation - Frequently Asked Questions (FAQs) for Implementing the Value Added Tax on E-Commerce Transactions, Cambodian General Department of Taxation - Questions and answers on value added tax, International Monetary Fund - Introducing Cambodia’s VAT on E-Commerce

%22%20fill%3D%22%23FFFFFF%22%3E%3Cpath%20d%3D%22M267.109551%2C33.9224%20L301.032051%2C0%20L334.954551%2C33.9224%20L329.125351%2C39.7516%20L301.032051%2C11.6583%20L272.938751%2C39.7516%20L267.109551%2C33.9224%20Z%20M322.483751%2C64.3549%20L338.106051%2C79.9772%20L332.276951%2C85.8064%20L316.654651%2C70.1841%20L301.032051%2C85.8064%20L267.109551%2C51.8839%20L272.938751%2C46.055%20L301.032051%2C74.1483%20L329.125351%2C46.055%20L334.954551%2C51.8839%20L322.483751%2C64.3549%20Z%22%20id%3D%22Fill-3%22%3E%3C%2Fpath%3E%3Cg%20id%3D%22v%22%20transform%3D%22translate(0%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpolygon%20id%3D%22Path%22%20points%3D%2223.1661333%200%2029.9750083%200%2018.1392686%2027.7674434%2011.8357397%2027.7674434%200%200%206.99505518%200%2015.0539971%2020.2404448%22%3E%3C%2Fpolygon%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(30.6833%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(65.3066%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(86.731%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22b%22%20transform%3D%22translate(123.2691%2C%2021.9462)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M15.9051064%2C10.7984502%20C18.4584346%2C10.7984502%2020.7812539%2C11.4323494%2022.8735645%2C12.7001477%20C24.965875%2C13.967946%2026.6060337%2C15.7144934%2027.7940405%2C17.9397898%20C28.9820474%2C20.1650862%2029.5760508%2C22.6341899%2029.5760508%2C25.3471011%20C29.5760508%2C28.0600122%2028.9820474%2C30.529116%2027.7940405%2C32.7544124%20C26.6060337%2C34.9797087%2024.965875%2C36.7262561%2022.8735645%2C37.9940544%20C20.7812539%2C39.2618528%2018.4584346%2C39.895752%2015.9051064%2C39.895752%20C13.8837217%2C39.895752%2012.0396514%2C39.4879287%2010.3728955%2C38.6722822%20C8.70613965%2C37.8566357%207.28762402%2C36.6952261%206.11734863%2C35.1880532%20L6.11734863%2C39.2308228%20L-5.68434189e-14%2C39.2308228%20L-5.68434189e-14%2C0%20L6.11734863%2C0%20L6.11734863%2C15.4795518%20C7.26989258%2C13.9901104%208.68397534%2C12.8375664%2010.3595969%2C12.0219199%20C12.0352185%2C11.2062734%2013.8837217%2C10.7984502%2015.9051064%2C10.7984502%20Z%20M8.56428809%2C31.517644%20C10.2133125%2C33.1666685%2012.2612944%2C33.9911807%2014.7082339%2C33.9911807%20C17.1551733%2C33.9911807%2019.1942896%2C33.1622356%2020.8255825%2C31.5043455%20C22.4568755%2C29.8464553%2023.272522%2C27.7940405%2023.272522%2C25.3471011%20C23.272522%2C22.9001616%2022.4568755%2C20.843314%2020.8255825%2C19.1765581%20C19.1942896%2C17.5098022%2017.1551733%2C16.6764243%2014.7082339%2C16.6764243%20C12.2612944%2C16.6764243%2010.2177454%2C17.5098022%208.57758667%2C19.1765581%20C6.93742798%2C20.843314%206.11734863%2C22.9001616%206.11734863%2C25.3471011%20C6.11734863%2C27.7940405%206.93299512%2C29.8508882%208.56428809%2C31.517644%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22o%22%20transform%3D%22translate(156.5624%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M14.8678169%2C29.0973018%20C10.6300015%2C29.0973018%207.09257812%2C27.7053833%204.25554687%2C24.9215464%20C1.41851562%2C22.1377095%200%2C18.6800776%200%2C14.5486509%20C0%2C10.4172241%201.41851562%2C6.95959229%204.25554687%2C4.17575537%20C7.09257812%2C1.39191846%2010.6300015%2C0%2014.8678169%2C0%20C17.6339224%2C0%2020.1562205%2C0.63389917%2022.4347112%2C1.90169751%20C24.7132019%2C3.16949585%2026.499645%2C4.91604321%2027.7940405%2C7.1413396%20C29.088436%2C9.36663599%2029.7356338%2C11.8357397%2029.7356338%2C14.5486509%20C29.7356338%2C17.261562%2029.088436%2C19.7306658%2027.7940405%2C21.9559622%20C26.499645%2C24.1812585%2024.7132019%2C25.9278059%2022.4347112%2C27.1956042%20C20.1562205%2C28.4634026%2017.6339224%2C29.0973018%2014.8678169%2C29.0973018%20Z%20M8.72387109%2C20.7191938%20C10.3728955%2C22.3682183%2012.4208774%2C23.1927305%2014.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.4208774%2C5.87797412%2010.3728955%2C6.71135205%208.72387109%2C8.37810791%20C7.07484668%2C10.0448638%206.25033447%2C12.1017114%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07484668%2C19.052438%208.72387109%2C20.7191938%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22u%22%20transform%3D%22translate(191.1474%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M12.8464321%2C28.4323726%20C8.98097705%2C28.4323726%205.87354126%2C27.3596201%203.52412476%2C25.2141152%20C1.17470825%2C23.0686104%200%2C20.2315791%200%2C16.7030215%20L0%2C0%20L6.09075146%2C0%20L6.09075146%2C15.9051064%20C6.09075146%2C17.8910283%206.71135205%2C19.4912913%207.95255322%2C20.7058953%20C9.19375439%2C21.9204993%2010.8250474%2C22.5278013%2012.8464321%2C22.5278013%20C14.8678169%2C22.5278013%2016.4902441%2C21.9249321%2017.7137139%2C20.7191938%20C18.9371836%2C19.5134556%2019.5489185%2C17.9087598%2019.5489185%2C15.9051064%20L19.5489185%2C0%20L25.6396699%2C0%20L25.6396699%2C16.7030215%20C25.6396699%2C20.2315791%2024.4693945%2C23.0686104%2022.1288437%2C25.2141152%20C19.788293%2C27.3596201%2016.6941558%2C28.4323726%2012.8464321%2C28.4323726%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(221.2498%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fsvg%3E)