%22%20fill%3D%22%23021A43%22%3E%3Cpath%20d%3D%22M267.109551%2C33.9224%20L301.032051%2C0%20L334.954551%2C33.9224%20L329.125351%2C39.7516%20L301.032051%2C11.6583%20L272.938751%2C39.7516%20L267.109551%2C33.9224%20Z%20M322.483751%2C64.3549%20L338.106051%2C79.9772%20L332.276951%2C85.8064%20L316.654651%2C70.1841%20L301.032051%2C85.8064%20L267.109551%2C51.8839%20L272.938751%2C46.055%20L301.032051%2C74.1483%20L329.125351%2C46.055%20L334.954551%2C51.8839%20L322.483751%2C64.3549%20Z%22%20id%3D%22Fill-3%22%3E%3C%2Fpath%3E%3Cg%20id%3D%22v%22%20transform%3D%22translate(0%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpolygon%20id%3D%22Path%22%20points%3D%2223.1661333%200%2029.9750083%200%2018.1392686%2027.7674434%2011.8357397%2027.7674434%200%200%206.99505518%200%2015.0539971%2020.2404448%22%3E%3C%2Fpolygon%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(30.6833%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(65.3066%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(86.731%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22b%22%20transform%3D%22translate(123.2691%2C%2021.9462)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M15.9051064%2C10.7984502%20C18.4584346%2C10.7984502%2020.7812539%2C11.4323494%2022.8735645%2C12.7001477%20C24.965875%2C13.967946%2026.6060337%2C15.7144934%2027.7940405%2C17.9397898%20C28.9820474%2C20.1650862%2029.5760508%2C22.6341899%2029.5760508%2C25.3471011%20C29.5760508%2C28.0600122%2028.9820474%2C30.529116%2027.7940405%2C32.7544124%20C26.6060337%2C34.9797087%2024.965875%2C36.7262561%2022.8735645%2C37.9940544%20C20.7812539%2C39.2618528%2018.4584346%2C39.895752%2015.9051064%2C39.895752%20C13.8837217%2C39.895752%2012.0396514%2C39.4879287%2010.3728955%2C38.6722822%20C8.70613965%2C37.8566357%207.28762402%2C36.6952261%206.11734863%2C35.1880532%20L6.11734863%2C39.2308228%20L-5.68434189e-14%2C39.2308228%20L-5.68434189e-14%2C0%20L6.11734863%2C0%20L6.11734863%2C15.4795518%20C7.26989258%2C13.9901104%208.68397534%2C12.8375664%2010.3595969%2C12.0219199%20C12.0352185%2C11.2062734%2013.8837217%2C10.7984502%2015.9051064%2C10.7984502%20Z%20M8.56428809%2C31.517644%20C10.2133125%2C33.1666685%2012.2612944%2C33.9911807%2014.7082339%2C33.9911807%20C17.1551733%2C33.9911807%2019.1942896%2C33.1622356%2020.8255825%2C31.5043455%20C22.4568755%2C29.8464553%2023.272522%2C27.7940405%2023.272522%2C25.3471011%20C23.272522%2C22.9001616%2022.4568755%2C20.843314%2020.8255825%2C19.1765581%20C19.1942896%2C17.5098022%2017.1551733%2C16.6764243%2014.7082339%2C16.6764243%20C12.2612944%2C16.6764243%2010.2177454%2C17.5098022%208.57758667%2C19.1765581%20C6.93742798%2C20.843314%206.11734863%2C22.9001616%206.11734863%2C25.3471011%20C6.11734863%2C27.7940405%206.93299512%2C29.8508882%208.56428809%2C31.517644%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22o%22%20transform%3D%22translate(156.5624%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M14.8678169%2C29.0973018%20C10.6300015%2C29.0973018%207.09257812%2C27.7053833%204.25554687%2C24.9215464%20C1.41851562%2C22.1377095%200%2C18.6800776%200%2C14.5486509%20C0%2C10.4172241%201.41851562%2C6.95959229%204.25554687%2C4.17575537%20C7.09257812%2C1.39191846%2010.6300015%2C0%2014.8678169%2C0%20C17.6339224%2C0%2020.1562205%2C0.63389917%2022.4347112%2C1.90169751%20C24.7132019%2C3.16949585%2026.499645%2C4.91604321%2027.7940405%2C7.1413396%20C29.088436%2C9.36663599%2029.7356338%2C11.8357397%2029.7356338%2C14.5486509%20C29.7356338%2C17.261562%2029.088436%2C19.7306658%2027.7940405%2C21.9559622%20C26.499645%2C24.1812585%2024.7132019%2C25.9278059%2022.4347112%2C27.1956042%20C20.1562205%2C28.4634026%2017.6339224%2C29.0973018%2014.8678169%2C29.0973018%20Z%20M8.72387109%2C20.7191938%20C10.3728955%2C22.3682183%2012.4208774%2C23.1927305%2014.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.4208774%2C5.87797412%2010.3728955%2C6.71135205%208.72387109%2C8.37810791%20C7.07484668%2C10.0448638%206.25033447%2C12.1017114%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07484668%2C19.052438%208.72387109%2C20.7191938%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22u%22%20transform%3D%22translate(191.1474%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M12.8464321%2C28.4323726%20C8.98097705%2C28.4323726%205.87354126%2C27.3596201%203.52412476%2C25.2141152%20C1.17470825%2C23.0686104%200%2C20.2315791%200%2C16.7030215%20L0%2C0%20L6.09075146%2C0%20L6.09075146%2C15.9051064%20C6.09075146%2C17.8910283%206.71135205%2C19.4912913%207.95255322%2C20.7058953%20C9.19375439%2C21.9204993%2010.8250474%2C22.5278013%2012.8464321%2C22.5278013%20C14.8678169%2C22.5278013%2016.4902441%2C21.9249321%2017.7137139%2C20.7191938%20C18.9371836%2C19.5134556%2019.5489185%2C17.9087598%2019.5489185%2C15.9051064%20L19.5489185%2C0%20L25.6396699%2C0%20L25.6396699%2C16.7030215%20C25.6396699%2C20.2315791%2024.4693945%2C23.0686104%2022.1288437%2C25.2141152%20C19.788293%2C27.3596201%2016.6941558%2C28.4323726%2012.8464321%2C28.4323726%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(221.2498%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fsvg%3E)

Over the past year or so, one of the main topics in the EU has been the VAT in the Digital Age (ViDA) reform and its impact not only on the EU VAT and e-invoicing system but also on the rise of global e-invoicing. For some time, the impact, significance, and scale of ViDA have been widely discussed, interpreted, and explained. However, at the heart of it lies the VAT gap: the hidden driver behind these sweeping changes, whose size, calculation, and implications are now crucial for every company operating in the digital economy.

What is the VAT Gap and Why Does it Matter?

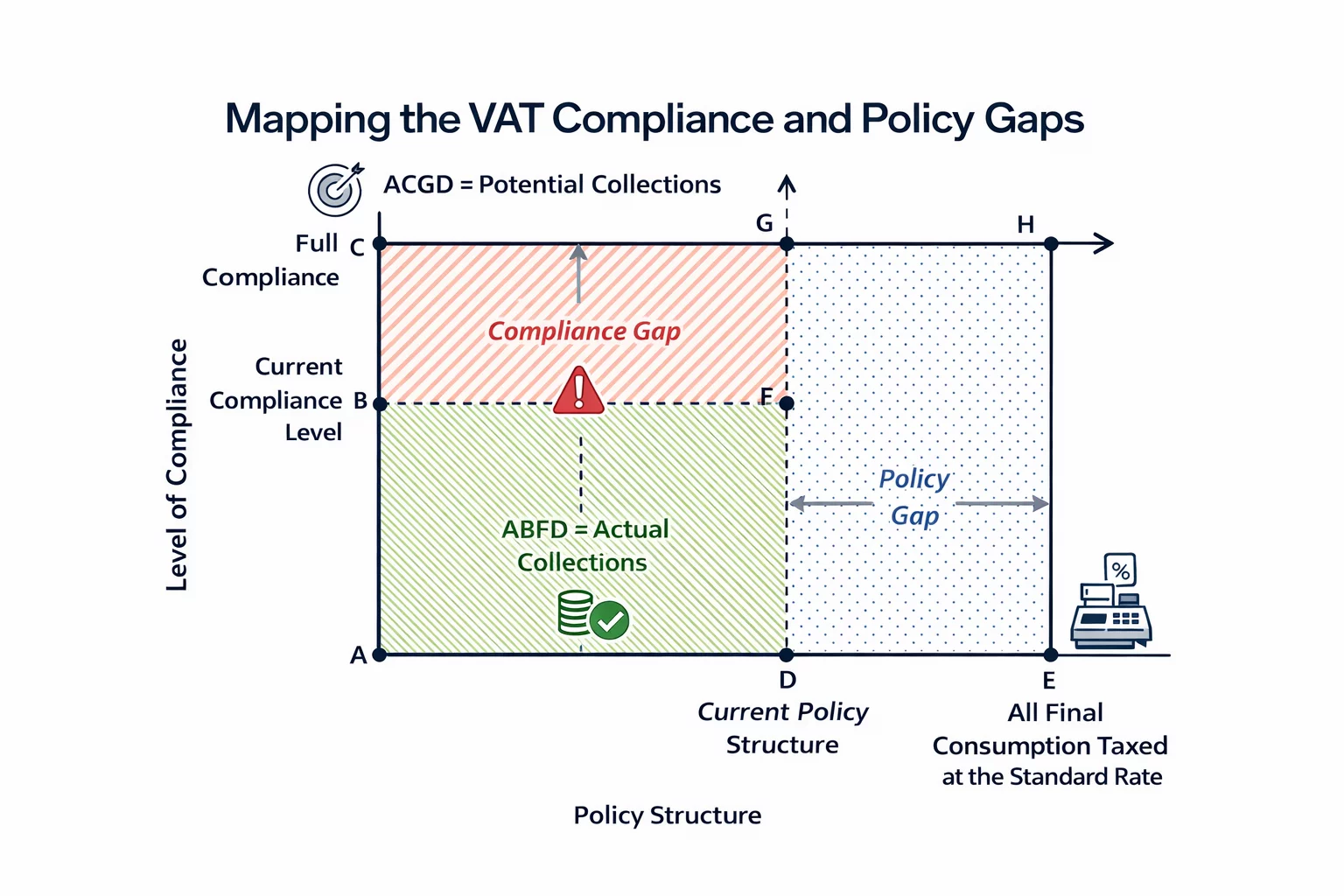

The VAT gap refers to the difference between the theoretical or potential VAT liability, that is, the total amount of VAT that should be collected if all transactions were perfectly compliant, and the VAT revenue actually collected by the tax authorities. In other words, the VAT gap represents a lost tax revenue and reflects how effectively a country’s tax system captures what is owed under current VAT laws.

Two main components that contribute to the VAT gap are the policy gap and the compliance gap. The policy gap arises from deliberate choices in tax law, such as exemptions, reduced rates, and thresholds intended to support social or economic goals. In contrast, the compliance gap represents the revenue lost due to non‑compliance with the law. The non-compliance can be due to evasion, fraud, bankruptcy, administrative errors, and other failures to pay due taxes.

Note: Data in the image is from the International Monetary Fund (IMF) - What is the VAT gap?

Considering that the VAT is a major source of revenue in many countries, e.g., EU countries raised over EUR 1,000 billion in VAT revenue, which represents 15.7% of total government tax revenue in 2023, any shortfalls in collection not only strain public budgets but also undermine economic policy goals and distort competition between compliant and non‑compliant taxable persons.

Measuring the Gap

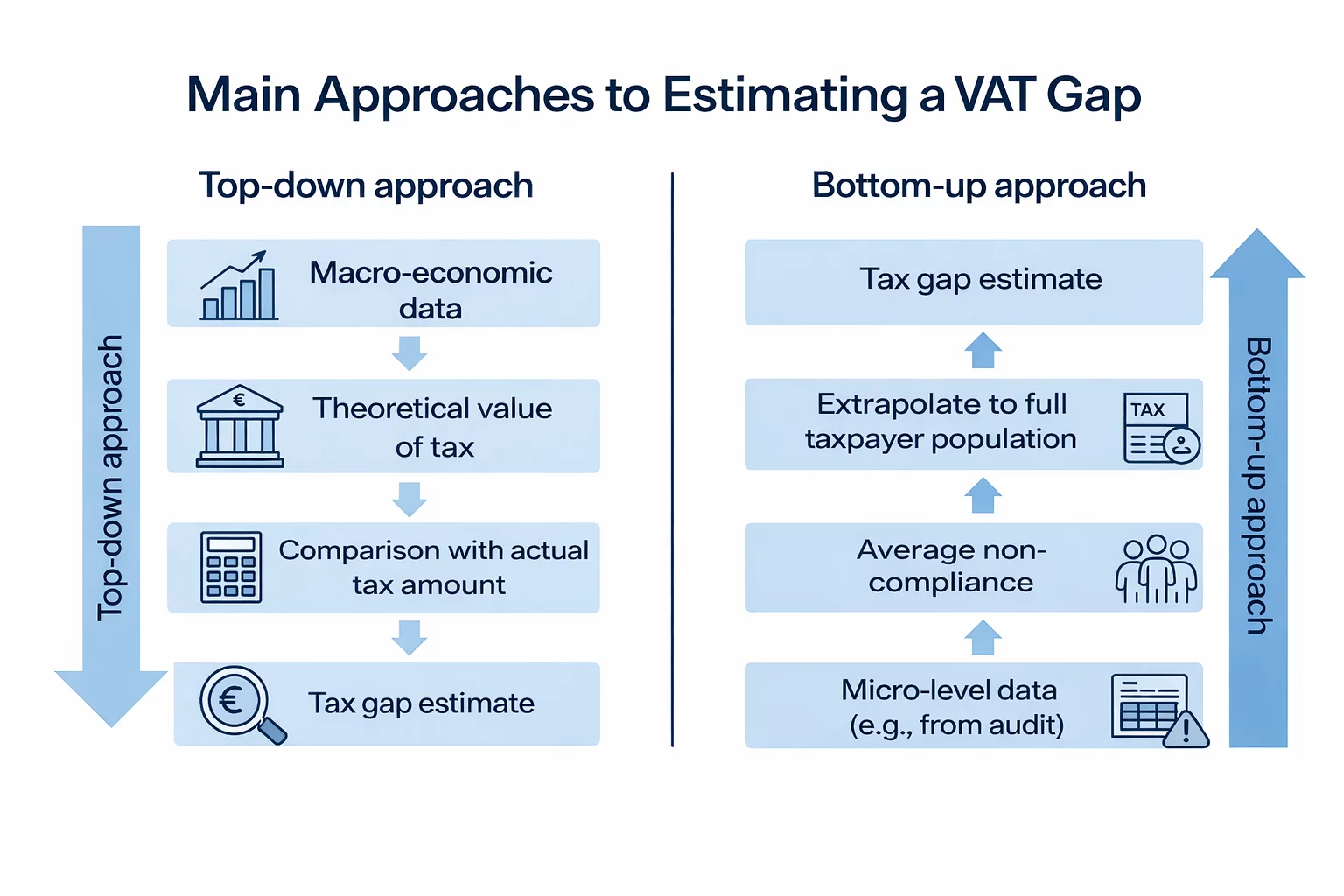

At first glance, measuring the VAT gap seems straightforward: estimate what should have been collected under full compliance, determine what was actually collected, and find the difference. In reality, calculating the VAT gap is an inherently complex exercise that requires careful analysis of both economic data and the behavior of taxable persons. To determine the gap, countries typically use one of two methodologies: the top-down or bottom-up approach.

The top-down approach relies on aggregate macroeconomic data, such as national statistics on total spending and income, to estimate how much tax should have been collected if everyone had followed the rules perfectly. By doing so, countries determine the theoretical amount of tax that the government expects to collect. Then that number is compared to the amount of tax actually collected, and the difference between the two amounts is considered the tax gap.

On the contrary, the bottom-up approach uses microeconomic data, i.e., detailed, real-life data from taxable persons. For example, Tax Authorities examine the results of audits, such as random or risk-based audits, to identify where and how much tax was underreported or unpaid. Based on that data, they estimate how widespread any specific kind of non-compliance is across the whole economy, and calculate the likely total tax gap.

Note: Data in the image is from the OECD Tax Administration 2024 report

In its Tax Administration 2024 report, the OECD noted that around 89% of countries use the top-down methodology. However, around 57% also apply bottom-up methods to complement their analysis. Notably, around 54% of countries rely on third-party support, such as the IMF, academic experts, Ministries of Finance, or independent consultants, to assist with estimating the tax gap.

What Lies Behind the VAT Gap Figures

While the VAT gap is commonly viewed as the revenue governments are losing, what it actually reveals goes deeper than a number. First, the VAT gap shows the level of tax compliance in a country. A small VAT gap generally indicates strong enforcement, efficient tax administration, and high levels of voluntary compliance. In contrast, a large gap suggests widespread non-compliance, whether due to fraud, evasion, insolvency, administrative errors, or weak enforcement.

Additionally, the results reflect the effectiveness of tax administration systems. For example, a constant or even growing VAT gap may result from outdated reporting systems, insufficient digital monitoring, or weak audit capacity. On the other hand, shrinking gaps often signal successful reforms such as e-invoicing, real-time reporting, or improved risk analysis.

Given that VAT is transaction-based, undeclared sales and informal economic activity directly increase the compliance gap. From that perspective, the VAT gap serves as an indirect indicator of the scale of the shadow economy.

When considering the broader context, including the policy gap, the VAT gap illustrates how exemptions, reduced rates, and thresholds shrink the potential tax base. These measures, while serving to achieve social or economic goals, shrink theoretical revenue capacity. This is known as the policy trade-off.

The Bottom Line: VAT Gaps and Business Operations

For businesses, the implications of VAT gaps are both direct and indirect. In countries with a large VAT gap, businesses that maintain high standards of VAT compliance may face competitive disadvantages relative to competitors who under‑report or evade tax. In other words, those that comply with VAT rules effectively carry a heavier share of the overall tax burden and may struggle to compete fairly in the market.

Non-compliance of other market participants can also prompt governments to impose tighter regulatory and enforcement regimes that increase administrative and compliance costs for all businesses, including compliant ones. In response to VAT gaps, the government may impose stringent reporting requirements, digital invoicing mandates, and enhanced auditing, pushing businesses to unplanned investments in robust tax accounting systems and compliance processes.

Following the EU's recent development of the deemed supplier rules, ViDA, and the overall reform of VAT and customs rules and regulations, the VAT gap led to stricter compliance frameworks, increased platform accountability, and a stronger push toward digitalisation and harmonised EU-wide reporting standards.

However, the effects are felt globally, resulting in a wave of new taxability rules and regulations for e-commerce and digital services. As a result, businesses engaged in cross-border supply must navigate diverse VAT regimes and enforcement practices.

Source: European Commission - EU VAT Gap Report, UK HM Revenue & Customs - Tax gaps: VAT, OECD - Tax Administration 2024, Australian Taxation Office, European Council - Value added tax (VAT) in the EU, EY, International Monetary Fund (IMF) - What is the VAT gap?

%22%20fill%3D%22%23FFFFFF%22%3E%3Cpath%20d%3D%22M267.109551%2C33.9224%20L301.032051%2C0%20L334.954551%2C33.9224%20L329.125351%2C39.7516%20L301.032051%2C11.6583%20L272.938751%2C39.7516%20L267.109551%2C33.9224%20Z%20M322.483751%2C64.3549%20L338.106051%2C79.9772%20L332.276951%2C85.8064%20L316.654651%2C70.1841%20L301.032051%2C85.8064%20L267.109551%2C51.8839%20L272.938751%2C46.055%20L301.032051%2C74.1483%20L329.125351%2C46.055%20L334.954551%2C51.8839%20L322.483751%2C64.3549%20Z%22%20id%3D%22Fill-3%22%3E%3C%2Fpath%3E%3Cg%20id%3D%22v%22%20transform%3D%22translate(0%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpolygon%20id%3D%22Path%22%20points%3D%2223.1661333%200%2029.9750083%200%2018.1392686%2027.7674434%2011.8357397%2027.7674434%200%200%206.99505518%200%2015.0539971%2020.2404448%22%3E%3C%2Fpolygon%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(30.6833%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(65.3066%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(86.731%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22b%22%20transform%3D%22translate(123.2691%2C%2021.9462)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M15.9051064%2C10.7984502%20C18.4584346%2C10.7984502%2020.7812539%2C11.4323494%2022.8735645%2C12.7001477%20C24.965875%2C13.967946%2026.6060337%2C15.7144934%2027.7940405%2C17.9397898%20C28.9820474%2C20.1650862%2029.5760508%2C22.6341899%2029.5760508%2C25.3471011%20C29.5760508%2C28.0600122%2028.9820474%2C30.529116%2027.7940405%2C32.7544124%20C26.6060337%2C34.9797087%2024.965875%2C36.7262561%2022.8735645%2C37.9940544%20C20.7812539%2C39.2618528%2018.4584346%2C39.895752%2015.9051064%2C39.895752%20C13.8837217%2C39.895752%2012.0396514%2C39.4879287%2010.3728955%2C38.6722822%20C8.70613965%2C37.8566357%207.28762402%2C36.6952261%206.11734863%2C35.1880532%20L6.11734863%2C39.2308228%20L-5.68434189e-14%2C39.2308228%20L-5.68434189e-14%2C0%20L6.11734863%2C0%20L6.11734863%2C15.4795518%20C7.26989258%2C13.9901104%208.68397534%2C12.8375664%2010.3595969%2C12.0219199%20C12.0352185%2C11.2062734%2013.8837217%2C10.7984502%2015.9051064%2C10.7984502%20Z%20M8.56428809%2C31.517644%20C10.2133125%2C33.1666685%2012.2612944%2C33.9911807%2014.7082339%2C33.9911807%20C17.1551733%2C33.9911807%2019.1942896%2C33.1622356%2020.8255825%2C31.5043455%20C22.4568755%2C29.8464553%2023.272522%2C27.7940405%2023.272522%2C25.3471011%20C23.272522%2C22.9001616%2022.4568755%2C20.843314%2020.8255825%2C19.1765581%20C19.1942896%2C17.5098022%2017.1551733%2C16.6764243%2014.7082339%2C16.6764243%20C12.2612944%2C16.6764243%2010.2177454%2C17.5098022%208.57758667%2C19.1765581%20C6.93742798%2C20.843314%206.11734863%2C22.9001616%206.11734863%2C25.3471011%20C6.11734863%2C27.7940405%206.93299512%2C29.8508882%208.56428809%2C31.517644%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22o%22%20transform%3D%22translate(156.5624%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M14.8678169%2C29.0973018%20C10.6300015%2C29.0973018%207.09257812%2C27.7053833%204.25554687%2C24.9215464%20C1.41851562%2C22.1377095%200%2C18.6800776%200%2C14.5486509%20C0%2C10.4172241%201.41851562%2C6.95959229%204.25554687%2C4.17575537%20C7.09257812%2C1.39191846%2010.6300015%2C0%2014.8678169%2C0%20C17.6339224%2C0%2020.1562205%2C0.63389917%2022.4347112%2C1.90169751%20C24.7132019%2C3.16949585%2026.499645%2C4.91604321%2027.7940405%2C7.1413396%20C29.088436%2C9.36663599%2029.7356338%2C11.8357397%2029.7356338%2C14.5486509%20C29.7356338%2C17.261562%2029.088436%2C19.7306658%2027.7940405%2C21.9559622%20C26.499645%2C24.1812585%2024.7132019%2C25.9278059%2022.4347112%2C27.1956042%20C20.1562205%2C28.4634026%2017.6339224%2C29.0973018%2014.8678169%2C29.0973018%20Z%20M8.72387109%2C20.7191938%20C10.3728955%2C22.3682183%2012.4208774%2C23.1927305%2014.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.4208774%2C5.87797412%2010.3728955%2C6.71135205%208.72387109%2C8.37810791%20C7.07484668%2C10.0448638%206.25033447%2C12.1017114%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07484668%2C19.052438%208.72387109%2C20.7191938%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22u%22%20transform%3D%22translate(191.1474%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M12.8464321%2C28.4323726%20C8.98097705%2C28.4323726%205.87354126%2C27.3596201%203.52412476%2C25.2141152%20C1.17470825%2C23.0686104%200%2C20.2315791%200%2C16.7030215%20L0%2C0%20L6.09075146%2C0%20L6.09075146%2C15.9051064%20C6.09075146%2C17.8910283%206.71135205%2C19.4912913%207.95255322%2C20.7058953%20C9.19375439%2C21.9204993%2010.8250474%2C22.5278013%2012.8464321%2C22.5278013%20C14.8678169%2C22.5278013%2016.4902441%2C21.9249321%2017.7137139%2C20.7191938%20C18.9371836%2C19.5134556%2019.5489185%2C17.9087598%2019.5489185%2C15.9051064%20L19.5489185%2C0%20L25.6396699%2C0%20L25.6396699%2C16.7030215%20C25.6396699%2C20.2315791%2024.4693945%2C23.0686104%2022.1288437%2C25.2141152%20C19.788293%2C27.3596201%2016.6941558%2C28.4323726%2012.8464321%2C28.4323726%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(221.2498%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fsvg%3E)