%22%20fill%3D%22%23021A43%22%3E%3Cpath%20d%3D%22M267.109551%2C33.9224%20L301.032051%2C0%20L334.954551%2C33.9224%20L329.125351%2C39.7516%20L301.032051%2C11.6583%20L272.938751%2C39.7516%20L267.109551%2C33.9224%20Z%20M322.483751%2C64.3549%20L338.106051%2C79.9772%20L332.276951%2C85.8064%20L316.654651%2C70.1841%20L301.032051%2C85.8064%20L267.109551%2C51.8839%20L272.938751%2C46.055%20L301.032051%2C74.1483%20L329.125351%2C46.055%20L334.954551%2C51.8839%20L322.483751%2C64.3549%20Z%22%20id%3D%22Fill-3%22%3E%3C%2Fpath%3E%3Cg%20id%3D%22v%22%20transform%3D%22translate(0%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpolygon%20id%3D%22Path%22%20points%3D%2223.1661333%200%2029.9750083%200%2018.1392686%2027.7674434%2011.8357397%2027.7674434%200%200%206.99505518%200%2015.0539971%2020.2404448%22%3E%3C%2Fpolygon%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(30.6833%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(65.3066%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(86.731%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22b%22%20transform%3D%22translate(123.2691%2C%2021.9462)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M15.9051064%2C10.7984502%20C18.4584346%2C10.7984502%2020.7812539%2C11.4323494%2022.8735645%2C12.7001477%20C24.965875%2C13.967946%2026.6060337%2C15.7144934%2027.7940405%2C17.9397898%20C28.9820474%2C20.1650862%2029.5760508%2C22.6341899%2029.5760508%2C25.3471011%20C29.5760508%2C28.0600122%2028.9820474%2C30.529116%2027.7940405%2C32.7544124%20C26.6060337%2C34.9797087%2024.965875%2C36.7262561%2022.8735645%2C37.9940544%20C20.7812539%2C39.2618528%2018.4584346%2C39.895752%2015.9051064%2C39.895752%20C13.8837217%2C39.895752%2012.0396514%2C39.4879287%2010.3728955%2C38.6722822%20C8.70613965%2C37.8566357%207.28762402%2C36.6952261%206.11734863%2C35.1880532%20L6.11734863%2C39.2308228%20L-5.68434189e-14%2C39.2308228%20L-5.68434189e-14%2C0%20L6.11734863%2C0%20L6.11734863%2C15.4795518%20C7.26989258%2C13.9901104%208.68397534%2C12.8375664%2010.3595969%2C12.0219199%20C12.0352185%2C11.2062734%2013.8837217%2C10.7984502%2015.9051064%2C10.7984502%20Z%20M8.56428809%2C31.517644%20C10.2133125%2C33.1666685%2012.2612944%2C33.9911807%2014.7082339%2C33.9911807%20C17.1551733%2C33.9911807%2019.1942896%2C33.1622356%2020.8255825%2C31.5043455%20C22.4568755%2C29.8464553%2023.272522%2C27.7940405%2023.272522%2C25.3471011%20C23.272522%2C22.9001616%2022.4568755%2C20.843314%2020.8255825%2C19.1765581%20C19.1942896%2C17.5098022%2017.1551733%2C16.6764243%2014.7082339%2C16.6764243%20C12.2612944%2C16.6764243%2010.2177454%2C17.5098022%208.57758667%2C19.1765581%20C6.93742798%2C20.843314%206.11734863%2C22.9001616%206.11734863%2C25.3471011%20C6.11734863%2C27.7940405%206.93299512%2C29.8508882%208.56428809%2C31.517644%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22o%22%20transform%3D%22translate(156.5624%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M14.8678169%2C29.0973018%20C10.6300015%2C29.0973018%207.09257812%2C27.7053833%204.25554687%2C24.9215464%20C1.41851562%2C22.1377095%200%2C18.6800776%200%2C14.5486509%20C0%2C10.4172241%201.41851562%2C6.95959229%204.25554687%2C4.17575537%20C7.09257812%2C1.39191846%2010.6300015%2C0%2014.8678169%2C0%20C17.6339224%2C0%2020.1562205%2C0.63389917%2022.4347112%2C1.90169751%20C24.7132019%2C3.16949585%2026.499645%2C4.91604321%2027.7940405%2C7.1413396%20C29.088436%2C9.36663599%2029.7356338%2C11.8357397%2029.7356338%2C14.5486509%20C29.7356338%2C17.261562%2029.088436%2C19.7306658%2027.7940405%2C21.9559622%20C26.499645%2C24.1812585%2024.7132019%2C25.9278059%2022.4347112%2C27.1956042%20C20.1562205%2C28.4634026%2017.6339224%2C29.0973018%2014.8678169%2C29.0973018%20Z%20M8.72387109%2C20.7191938%20C10.3728955%2C22.3682183%2012.4208774%2C23.1927305%2014.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.4208774%2C5.87797412%2010.3728955%2C6.71135205%208.72387109%2C8.37810791%20C7.07484668%2C10.0448638%206.25033447%2C12.1017114%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07484668%2C19.052438%208.72387109%2C20.7191938%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22u%22%20transform%3D%22translate(191.1474%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M12.8464321%2C28.4323726%20C8.98097705%2C28.4323726%205.87354126%2C27.3596201%203.52412476%2C25.2141152%20C1.17470825%2C23.0686104%200%2C20.2315791%200%2C16.7030215%20L0%2C0%20L6.09075146%2C0%20L6.09075146%2C15.9051064%20C6.09075146%2C17.8910283%206.71135205%2C19.4912913%207.95255322%2C20.7058953%20C9.19375439%2C21.9204993%2010.8250474%2C22.5278013%2012.8464321%2C22.5278013%20C14.8678169%2C22.5278013%2016.4902441%2C21.9249321%2017.7137139%2C20.7191938%20C18.9371836%2C19.5134556%2019.5489185%2C17.9087598%2019.5489185%2C15.9051064%20L19.5489185%2C0%20L25.6396699%2C0%20L25.6396699%2C16.7030215%20C25.6396699%2C20.2315791%2024.4693945%2C23.0686104%2022.1288437%2C25.2141152%20C19.788293%2C27.3596201%2016.6941558%2C28.4323726%2012.8464321%2C28.4323726%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(221.2498%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fsvg%3E)

The tax gap and high tax administration costs are the two most important challenges facing tax departments worldwide. The tax gap refers to the difference between actual taxes collected and taxes that should have been collected. The primary reason for the tax gap is tax evasion and avoidance, false refund claims, and underreporting of sales.

In a 2022 report, the US tax department estimated a loss of USD 606 billion in tax revenue due to the tax gap. This accounts for 2.33% of the US GDP of 2022. Considering the same ratio to the world GDP of USD 110 trillion by 2024, the loss is estimated to be USD 2.56 trillion. If we add a higher margin for underdeveloped and developing countries, it can go as high as USD 4 trillion.

High tax administration costs are associated with costs incurred by tax departments with tax registration, record keeping, transaction verification, tax assessment, collection, and dispute resolution. These activities are time and resource-consuming.

Blockchain technology has emerged as a transformative solution for the modern tax administration. The key characteristics of blockchain technology, like transparency, immutability, and decentralization, facilitate real-time reporting at the transactional level. It can perform automatic tax validation and computation of taxes using smart contracts. It can enable tax payment per transaction and improve cross-border collaboration. Some tax departments around the world that have implemented blockchain have demonstrated higher efficiency in tax collection and lower operating costs.

However, incorporating blockchain technology goes beyond just a technological change. It requires regulatory changes, system upgrades, organizational changes for both taxpayers and tax authorities, and building digital infrastructure.

Blockchain Overview

Blockchain is a digital ledger, just like a traditional accounting book. Every transaction in blockchain is verified, and real-time copies of the ledger are shared among the participating computers called nodes. Blockchain is also known as Distributed Ledger Technology (DLT).

Blockchain is a combination of two words, block and chain. Every transaction initiated in the blockchain technology is verified by the participant nodes. The transactions that are successfully verified are collected and converted into a block. Each block is added to the ledger by connecting with the previous block like a chain using advanced cryptography. Once a transaction is added to the blockchain, it cannot be altered, removed, or amended without the permission of all participating nodes, hence making this a permanent record. The key characteristics of blockchain technology are decentralized, transparent, immutable, and secure.

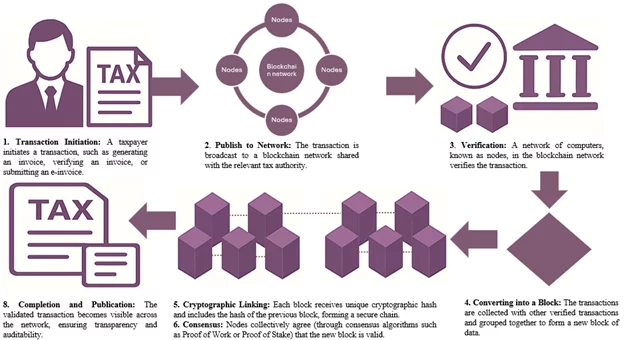

The blockchain process works as follows:

- Transaction Initiation: A taxpayer initiates a taxable transaction and submits it to blockchain technology via a digital invoice or a common technology platform.

- Published to Network: The transaction is securely shared with the tax authority for verification.

- Validate by participating nodes: The tax authority verifies the transaction, like Taxpayer details, Customer/Vendor information, underlying goods/service details, price per unit, tax calculation, etc.

- Converting into a Block: Once the transaction is verified, it will form a new block of data.

- Cryptographic Link: Each new block receives a unique cryptographic hash that includes the hash of the preceding block. It ensures an unbroken and secure chain of blocks.

- Consensus: Each participant node agrees that the new block is valid.

- Added and published: The new block is permanently added to the ledger, and a copy of the record is shared with participant nodes, e.g., the taxpayer and the tax authority, in real-time.

Fig 1: Blockchain Process

Types of Blockchain Systems

Blockchain is broadly classified into three categories based on access control and governance structure:

- Public Blockchain: Public blockchains are permissionless and fully decentralized. Anyone can participate, view transactions, and host a copy of the ledger. Cryptocurrencies like Bitcoin and Ethereum are examples of public blockchains.

- Private Blockchain: Private blockchains are permissioned and controlled by one or more centralized entities. Only authorized participants can initiate, validate, view, and hold a copy of the ledger. This is a more protected and secure blockchain technology. This is ideal for government and enterprise user cases.

- Consortium or Hybrid Blockchain: This represents a mix of Public and Private Blockchain. They are semi-decentralized but provide transparency and control. This type is best suited for inter-agency or multi-jurisdictional tax authorities

Private or Consortium is the most ideal blockchain technology for tax administration. This provides better control, security, and performance.

Model of Blockchain Technology in Tax Administration

Blockchain technology can transform tax administration by bringing transparency, automation, and immutability. It can be used in tax administration in its simplest form of sharing tax data in real-time, to an advanced use case of automating tax calculation, tax payment, and artificial intelligence (AI).

Two advanced models of blockchain technology in taxation are discussed here. The first model automates tax compliance through blockchain by integrating tax calculation and settlement as part of the process. The second one further advances the model by incorporating AI into the process.

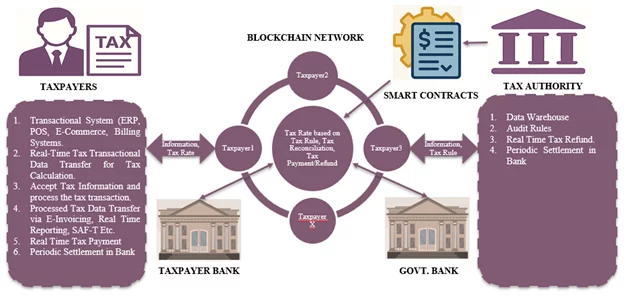

Tax Compliance Through Blockchain: Integrating Calculation and Settlement

This model is based on the three features of blockchain technology: real-time data sharing, smart contracts, and executing digital currency transactions.

Blockchain technology facilitates the sharing of tax data in real-time with the tax authority. This makes the entire process more transparent and eliminates the need for periodic reporting. Blockchain can automate tax calculation by integrating smart contracts into the process. Smart contracts execute automatically once certain preconditions are met.

Tax authorities can publish tax rules and rates in the blockchain network using smart contracts. Any transaction initiated by the taxpayer will be validated against these contracts for tax rates. The process can be further enhanced by integrating cryptocurrency into tax systems. In fact, the blockchain was originally designed to transfer digital currencies without the involvement of central banks. The same mechanism can be applied here.

Tax payments can be settled via a nominated digital currency using smart contracts. These contracts can automatically execute to process tax payments and refunds, including input tax credit, if certain preconditions are met. For example, a refund can be held in an escrow account until the underlying transaction is validated via a counterparty transaction. Periodically, the digital asset can be settled with a bank. This entire process will reduce errors, administrative workload, and processing time.

Below is the step-by-step process:

- Transaction Creation: The taxpayer’s systems, such as ERP, procurement, e-commerce, or billing platforms, initiate taxable transactions.

- Real-Time transaction shared: The transaction is shared to the blockchain network in real time.

- Secure Identity Management: Taxpayer identification is secured through cryptographic keys. Each taxpayer can access only its own account, while tax authorities can monitor all accounts.

- Smart Contract: The tax rules and rates are published by tax authorities on a blockchain network using smart contracts. The transaction is validated against the smart contracts. The tax rates are sent back for successfully executed transactions. The failure reason is communicated for failed transactions, like a missing tax registration number, etc.

- Tax Rate acceptance: The taxpayer’s system accepts the tax rate and processes the tax transaction in the taxpayer’s system.

- Real-Time Reporting: The processed transaction is shared in real time using accepted frameworks, like SAF-T (Standard Audit File for Taxation), or E-Invoicing.

- Automated Audits and Reconciliation: Tax and audit rules are built into the tax authority system. Every shared transaction is verified immediately against these rules. Any audit findings are communicated back to the taxpayer.

- Automated Payment/Refund: Payments and refunds are processed per transaction using cryptocurrency. Refunds may be held in escrow until the corresponding counterparty transaction is confirmed.

- Periodical reconciliation: Authorities and taxpayers can reconcile data at set intervals, ensuring completeness and accuracy.

- Bank Settlement: Cryptocurrency-based payments are periodically settled through traditional banking channels.

- Elimination for Traditional Returns: Since the system receives, monitors, verifies, and reconciles taxes in real-time, taxpayers no longer need to file traditional periodic tax returns.

Fig 2: Tax Compliance Through Blockchain: Integrating Calculation and Settlement

Intelligent Tax Systems: AI and Blockchain for an Autonomous Tax System

Artificial Intelligence (AI) and Blockchain are two advanced technologies. Together, they can create a secure, smart, and self-checking tax system. This will be an “autonomous tax compliance” system that automatically assesses and adjusts taxes based on changing laws and transactions. It will reduce dependency on manual processes and ensure that taxes are collected and reported in real-time. Integrating AI into the blockchain-based tax system will add intelligence and make the system smarter. AI can help in ensuring data accuracy, predictive analytics, tax calculation, and trend analysis.

Below are the use cases of integrating AI into blockchain:

Steps | Taxpayer (Business / Individual) & AI | Blockchain & AI Technology Layer | Tax Authority (Government / Regulator) & AI |

Data Collection & Validation | Data cleansing and classification of tax-relevant transactions. | Validates and structures data. Flags anomalies before posting to the ledger. | Monitor and validate data consistency across taxpayers. |

Smart Contract Activation | -- | -- | Automatically update smart contracts based on new regulations. |

Tax Determination & Calculation | Determines applicable tax codes and rates. | Performs real-time tax computation and prediction. | Reviews computed taxes in real time, reducing manual audits. |

Filing & Compliance Reporting | Assists in error detection and reconciliation. Submits auto-generated returns. | Auto-generates compliance reports and identifies inconsistencies. | Automatically reconciles taxpayer data with blockchain records. Uses AI to cross-check filings across taxpayers. |

Payment & Settlement | Uses AI for cash flow forecasting and payment scheduling into the blockchain network. | Confirms payment accuracy and updates ledgers. | Confirm payment accuracy and receive payment instantly via blockchain transaction validation. |

Fraud Detection & Risk Management | Uses AI tools to monitor internal controls and detect fraudulent invoices. | Identifies patterns of high-risk behavior. | Deploys AI analytics to detect fraud, underreporting, or duplicate claims. |

Continuous Monitoring & Learning | Receives AI reports on tax performance and compliance trends. | Optimize compliance and predict risks. | Adjust policies based on real-time analytics and AI-driven forecasts. |

Implementation Requirements

Implementing blockchain in tax systems is a complex undertaking. It requires changes across stakeholders, regulatory policies, technology infrastructure, and data security.

Regulatory Considerations

The Government must update tax laws and regulations to recognize blockchain-based transactions and smart contracts as legally valid. The new frameworks should include regulation for automated tax processes, digital payments, and real-time reporting requirements.

People and Change Management

Any implementation fails without proper adoption by its users. Effective change management must address any resistance from both tax authorities and taxpayers. The government must collect feedback and suggestions. Every step of the process must be clear and explained well to avoid any ambiguity. The government should also support taxpayers, especially small taxpayers, in adopting new technology by offering tax incentives, training, awareness, and, in some situations, monetary assistance.

Technological Infrastructure

The government needs to establish a secure, reliable, and scalable IT infrastructure based on blockchain technology that can process a large volume of transactions in real-time, especially during peak periods. The government must adopt or establish a standardized data format, like SAF-T or E-Invoicing. Furthermore, the system must be bidirectional so that data can be exchanged freely between taxpayers and tax authorities. Finally, the system must be integrated with a digital payment system, either via cryptocurrency or any other form of digital payment, to facilitate real-time tax payment and refunds.

Security and Data Protection

Tax data is very sensitive and important. It must be protected by implementing strong security measures. The blockchain system must be either private or Consortium. Each taxpayer must identify through a secure identification method, like a digital identifier or cryptographic key. The tax data must be restricted. Each taxpayer can only access their own data, and the tax authority can access tax data for all taxpayers. Strict cybersecurity and data protection standards must be adopted to safeguard the tax data.

Benefits

Blockchain technology in taxation offers advantages to both taxpayers and tax authorities.

Tax Authorities

Blockchain improves the operational and administrative efficiency of tax authorities by automating key functions such as transaction verification, recordkeeping, tax assessment, real-time audit, and tax collection. This will reduce the overall operational cost to the tax authorities. It also allows tax officials to spend more time on strategy and policy frameworks rather than on administrative tasks. Blockchain ledger records are immutable, chronological, and have a clear audit trail. This improves the overall audit effectiveness and reduces the inaccuracies in tax transactions.

The blockchain also provides greater transparency and helps detect fraudulent activities. Real-time validation and integrating it with the payment system allows quicker collection of taxes. It reduces the tax gap by reducing revenue leakage. In addition, it improves coordination among various tax authorities and taxpayers. It reduces corruption and strengthens public trust in government.

Taxpayer

Blockchain simplifies tax compliance and reduces the overall tax administrative cost. Smart contracts can automate the calculation or verification of taxes, ensuring accuracy and reducing human error. Real-time data sharing and validation help taxpayers to spend less time and money on periodic tax returns and reconciliations. Tax payments and refunds are processed in real time. This will improve cash flow. Due to a clear audit trail, taxpayers can real-time track the status of every transaction in the system. The records are saved in an immutable journal. This will bring greater transparency, mutual trust, and confidence in the system.

System-Level Benefits

At the macro level, blockchain brings more transparency to the tax ecosystem. This helps in bringing informal transactions into the formal economy and reduces the tax gap. Direct exchange of information between governments and taxpayers eliminates intermediaries and transactional costs. Blockchain provides a permanent, secure, and immutable record of all economic activities of the country.

Blockchain can further expand to share information between various tax authorities within the country. This will increase overall tax compliance and reduce redundant reporting requirements. Blockchain can be enabled for cross-border transactions for better visibility and to reduce fraud. This will improve international coordination and global tax compliance.

Overall, blockchain adoption in taxation not only improves efficiency and reduces costs but also fosters trust, accountability, and transparency, creating a more robust and compliant tax ecosystem.

Challenges

Implementing a system based on blockchain comes with several challenges. One of the biggest challenges is managing change across stakeholders. The resistance to new processes and limited digital literacy can slow adoption. The new system must integrate with legacy IT systems and databases. This requires a significant investment from both taxpayers and tax authorities. Blockchain is a more open and transparent system.

Cybersecurity, data privacy, and protection will remain a major concern for this technology. Introducing smart contracts and digital payments requires high technology costs and cooperation from various government departments.

The regulatory and Policy gaps must be addressed before implementation. Additionally, systems can struggle during peak time due to the high volume of transactions, so scalability and resource limitations must be addressed to fully realize the potential of the blockchain in taxation. International collaboration is needed for cross-border transactions.

Conclusion

Blockchain technology presents a solution to address the long-standing inefficiencies in tax administration. Blockchain can streamline tax processes by enabling real-time data collection and verification, automating tax calculation. It can record data in an immutable ledger and facilitate tax collection per transaction. According to one study, blockchain could reduce the tax gap by 70–80% and administrative costs by 40–50%.

When integrating with AI, it can create an “autonomous tax compliance” system that automatically assesses and adjusts taxes based on changing laws and transaction patterns. However, creating a system based on blockchain is complex. It requires a change in regulatory policies, technology infrastructure, and adoption by both taxpayers and tax authorities.

Despite these challenges, the benefits outweigh the hurdles. A system based on blockchain promises greater transparency, efficiency, and trust. This will ultimately transform the taxation system into a fairer, secure, and future-ready system.

Source: Penn State Law Review, Internal Revenue Service, World Bank, PwC, FasterCapital, International Journal of Science and Research, Computer Science & IT Research Journal, European Journal of Scientific Research and Reviews

%22%20fill%3D%22%23FFFFFF%22%3E%3Cpath%20d%3D%22M267.109551%2C33.9224%20L301.032051%2C0%20L334.954551%2C33.9224%20L329.125351%2C39.7516%20L301.032051%2C11.6583%20L272.938751%2C39.7516%20L267.109551%2C33.9224%20Z%20M322.483751%2C64.3549%20L338.106051%2C79.9772%20L332.276951%2C85.8064%20L316.654651%2C70.1841%20L301.032051%2C85.8064%20L267.109551%2C51.8839%20L272.938751%2C46.055%20L301.032051%2C74.1483%20L329.125351%2C46.055%20L334.954551%2C51.8839%20L322.483751%2C64.3549%20Z%22%20id%3D%22Fill-3%22%3E%3C%2Fpath%3E%3Cg%20id%3D%22v%22%20transform%3D%22translate(0%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpolygon%20id%3D%22Path%22%20points%3D%2223.1661333%200%2029.9750083%200%2018.1392686%2027.7674434%2011.8357397%2027.7674434%200%200%206.99505518%200%2015.0539971%2020.2404448%22%3E%3C%2Fpolygon%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(30.6833%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(65.3066%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(86.731%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22b%22%20transform%3D%22translate(123.2691%2C%2021.9462)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M15.9051064%2C10.7984502%20C18.4584346%2C10.7984502%2020.7812539%2C11.4323494%2022.8735645%2C12.7001477%20C24.965875%2C13.967946%2026.6060337%2C15.7144934%2027.7940405%2C17.9397898%20C28.9820474%2C20.1650862%2029.5760508%2C22.6341899%2029.5760508%2C25.3471011%20C29.5760508%2C28.0600122%2028.9820474%2C30.529116%2027.7940405%2C32.7544124%20C26.6060337%2C34.9797087%2024.965875%2C36.7262561%2022.8735645%2C37.9940544%20C20.7812539%2C39.2618528%2018.4584346%2C39.895752%2015.9051064%2C39.895752%20C13.8837217%2C39.895752%2012.0396514%2C39.4879287%2010.3728955%2C38.6722822%20C8.70613965%2C37.8566357%207.28762402%2C36.6952261%206.11734863%2C35.1880532%20L6.11734863%2C39.2308228%20L-5.68434189e-14%2C39.2308228%20L-5.68434189e-14%2C0%20L6.11734863%2C0%20L6.11734863%2C15.4795518%20C7.26989258%2C13.9901104%208.68397534%2C12.8375664%2010.3595969%2C12.0219199%20C12.0352185%2C11.2062734%2013.8837217%2C10.7984502%2015.9051064%2C10.7984502%20Z%20M8.56428809%2C31.517644%20C10.2133125%2C33.1666685%2012.2612944%2C33.9911807%2014.7082339%2C33.9911807%20C17.1551733%2C33.9911807%2019.1942896%2C33.1622356%2020.8255825%2C31.5043455%20C22.4568755%2C29.8464553%2023.272522%2C27.7940405%2023.272522%2C25.3471011%20C23.272522%2C22.9001616%2022.4568755%2C20.843314%2020.8255825%2C19.1765581%20C19.1942896%2C17.5098022%2017.1551733%2C16.6764243%2014.7082339%2C16.6764243%20C12.2612944%2C16.6764243%2010.2177454%2C17.5098022%208.57758667%2C19.1765581%20C6.93742798%2C20.843314%206.11734863%2C22.9001616%206.11734863%2C25.3471011%20C6.11734863%2C27.7940405%206.93299512%2C29.8508882%208.56428809%2C31.517644%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22o%22%20transform%3D%22translate(156.5624%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M14.8678169%2C29.0973018%20C10.6300015%2C29.0973018%207.09257812%2C27.7053833%204.25554687%2C24.9215464%20C1.41851562%2C22.1377095%200%2C18.6800776%200%2C14.5486509%20C0%2C10.4172241%201.41851562%2C6.95959229%204.25554687%2C4.17575537%20C7.09257812%2C1.39191846%2010.6300015%2C0%2014.8678169%2C0%20C17.6339224%2C0%2020.1562205%2C0.63389917%2022.4347112%2C1.90169751%20C24.7132019%2C3.16949585%2026.499645%2C4.91604321%2027.7940405%2C7.1413396%20C29.088436%2C9.36663599%2029.7356338%2C11.8357397%2029.7356338%2C14.5486509%20C29.7356338%2C17.261562%2029.088436%2C19.7306658%2027.7940405%2C21.9559622%20C26.499645%2C24.1812585%2024.7132019%2C25.9278059%2022.4347112%2C27.1956042%20C20.1562205%2C28.4634026%2017.6339224%2C29.0973018%2014.8678169%2C29.0973018%20Z%20M8.72387109%2C20.7191938%20C10.3728955%2C22.3682183%2012.4208774%2C23.1927305%2014.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.4208774%2C5.87797412%2010.3728955%2C6.71135205%208.72387109%2C8.37810791%20C7.07484668%2C10.0448638%206.25033447%2C12.1017114%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07484668%2C19.052438%208.72387109%2C20.7191938%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22u%22%20transform%3D%22translate(191.1474%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M12.8464321%2C28.4323726%20C8.98097705%2C28.4323726%205.87354126%2C27.3596201%203.52412476%2C25.2141152%20C1.17470825%2C23.0686104%200%2C20.2315791%200%2C16.7030215%20L0%2C0%20L6.09075146%2C0%20L6.09075146%2C15.9051064%20C6.09075146%2C17.8910283%206.71135205%2C19.4912913%207.95255322%2C20.7058953%20C9.19375439%2C21.9204993%2010.8250474%2C22.5278013%2012.8464321%2C22.5278013%20C14.8678169%2C22.5278013%2016.4902441%2C21.9249321%2017.7137139%2C20.7191938%20C18.9371836%2C19.5134556%2019.5489185%2C17.9087598%2019.5489185%2C15.9051064%20L19.5489185%2C0%20L25.6396699%2C0%20L25.6396699%2C16.7030215%20C25.6396699%2C20.2315791%2024.4693945%2C23.0686104%2022.1288437%2C25.2141152%20C19.788293%2C27.3596201%2016.6941558%2C28.4323726%2012.8464321%2C28.4323726%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(221.2498%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fsvg%3E)