%22%20fill%3D%22%23021A43%22%3E%3Cpath%20d%3D%22M267.109551%2C33.9224%20L301.032051%2C0%20L334.954551%2C33.9224%20L329.125351%2C39.7516%20L301.032051%2C11.6583%20L272.938751%2C39.7516%20L267.109551%2C33.9224%20Z%20M322.483751%2C64.3549%20L338.106051%2C79.9772%20L332.276951%2C85.8064%20L316.654651%2C70.1841%20L301.032051%2C85.8064%20L267.109551%2C51.8839%20L272.938751%2C46.055%20L301.032051%2C74.1483%20L329.125351%2C46.055%20L334.954551%2C51.8839%20L322.483751%2C64.3549%20Z%22%20id%3D%22Fill-3%22%3E%3C%2Fpath%3E%3Cg%20id%3D%22v%22%20transform%3D%22translate(0%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpolygon%20id%3D%22Path%22%20points%3D%2223.1661333%200%2029.9750083%200%2018.1392686%2027.7674434%2011.8357397%2027.7674434%200%200%206.99505518%200%2015.0539971%2020.2404448%22%3E%3C%2Fpolygon%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(30.6833%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(65.3066%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(86.731%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22b%22%20transform%3D%22translate(123.2691%2C%2021.9462)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M15.9051064%2C10.7984502%20C18.4584346%2C10.7984502%2020.7812539%2C11.4323494%2022.8735645%2C12.7001477%20C24.965875%2C13.967946%2026.6060337%2C15.7144934%2027.7940405%2C17.9397898%20C28.9820474%2C20.1650862%2029.5760508%2C22.6341899%2029.5760508%2C25.3471011%20C29.5760508%2C28.0600122%2028.9820474%2C30.529116%2027.7940405%2C32.7544124%20C26.6060337%2C34.9797087%2024.965875%2C36.7262561%2022.8735645%2C37.9940544%20C20.7812539%2C39.2618528%2018.4584346%2C39.895752%2015.9051064%2C39.895752%20C13.8837217%2C39.895752%2012.0396514%2C39.4879287%2010.3728955%2C38.6722822%20C8.70613965%2C37.8566357%207.28762402%2C36.6952261%206.11734863%2C35.1880532%20L6.11734863%2C39.2308228%20L-5.68434189e-14%2C39.2308228%20L-5.68434189e-14%2C0%20L6.11734863%2C0%20L6.11734863%2C15.4795518%20C7.26989258%2C13.9901104%208.68397534%2C12.8375664%2010.3595969%2C12.0219199%20C12.0352185%2C11.2062734%2013.8837217%2C10.7984502%2015.9051064%2C10.7984502%20Z%20M8.56428809%2C31.517644%20C10.2133125%2C33.1666685%2012.2612944%2C33.9911807%2014.7082339%2C33.9911807%20C17.1551733%2C33.9911807%2019.1942896%2C33.1622356%2020.8255825%2C31.5043455%20C22.4568755%2C29.8464553%2023.272522%2C27.7940405%2023.272522%2C25.3471011%20C23.272522%2C22.9001616%2022.4568755%2C20.843314%2020.8255825%2C19.1765581%20C19.1942896%2C17.5098022%2017.1551733%2C16.6764243%2014.7082339%2C16.6764243%20C12.2612944%2C16.6764243%2010.2177454%2C17.5098022%208.57758667%2C19.1765581%20C6.93742798%2C20.843314%206.11734863%2C22.9001616%206.11734863%2C25.3471011%20C6.11734863%2C27.7940405%206.93299512%2C29.8508882%208.56428809%2C31.517644%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22o%22%20transform%3D%22translate(156.5624%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M14.8678169%2C29.0973018%20C10.6300015%2C29.0973018%207.09257812%2C27.7053833%204.25554687%2C24.9215464%20C1.41851562%2C22.1377095%200%2C18.6800776%200%2C14.5486509%20C0%2C10.4172241%201.41851562%2C6.95959229%204.25554687%2C4.17575537%20C7.09257812%2C1.39191846%2010.6300015%2C0%2014.8678169%2C0%20C17.6339224%2C0%2020.1562205%2C0.63389917%2022.4347112%2C1.90169751%20C24.7132019%2C3.16949585%2026.499645%2C4.91604321%2027.7940405%2C7.1413396%20C29.088436%2C9.36663599%2029.7356338%2C11.8357397%2029.7356338%2C14.5486509%20C29.7356338%2C17.261562%2029.088436%2C19.7306658%2027.7940405%2C21.9559622%20C26.499645%2C24.1812585%2024.7132019%2C25.9278059%2022.4347112%2C27.1956042%20C20.1562205%2C28.4634026%2017.6339224%2C29.0973018%2014.8678169%2C29.0973018%20Z%20M8.72387109%2C20.7191938%20C10.3728955%2C22.3682183%2012.4208774%2C23.1927305%2014.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.4208774%2C5.87797412%2010.3728955%2C6.71135205%208.72387109%2C8.37810791%20C7.07484668%2C10.0448638%206.25033447%2C12.1017114%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07484668%2C19.052438%208.72387109%2C20.7191938%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22u%22%20transform%3D%22translate(191.1474%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M12.8464321%2C28.4323726%20C8.98097705%2C28.4323726%205.87354126%2C27.3596201%203.52412476%2C25.2141152%20C1.17470825%2C23.0686104%200%2C20.2315791%200%2C16.7030215%20L0%2C0%20L6.09075146%2C0%20L6.09075146%2C15.9051064%20C6.09075146%2C17.8910283%206.71135205%2C19.4912913%207.95255322%2C20.7058953%20C9.19375439%2C21.9204993%2010.8250474%2C22.5278013%2012.8464321%2C22.5278013%20C14.8678169%2C22.5278013%2016.4902441%2C21.9249321%2017.7137139%2C20.7191938%20C18.9371836%2C19.5134556%2019.5489185%2C17.9087598%2019.5489185%2C15.9051064%20L19.5489185%2C0%20L25.6396699%2C0%20L25.6396699%2C16.7030215%20C25.6396699%2C20.2315791%2024.4693945%2C23.0686104%2022.1288437%2C25.2141152%20C19.788293%2C27.3596201%2016.6941558%2C28.4323726%2012.8464321%2C28.4323726%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(221.2498%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fsvg%3E)

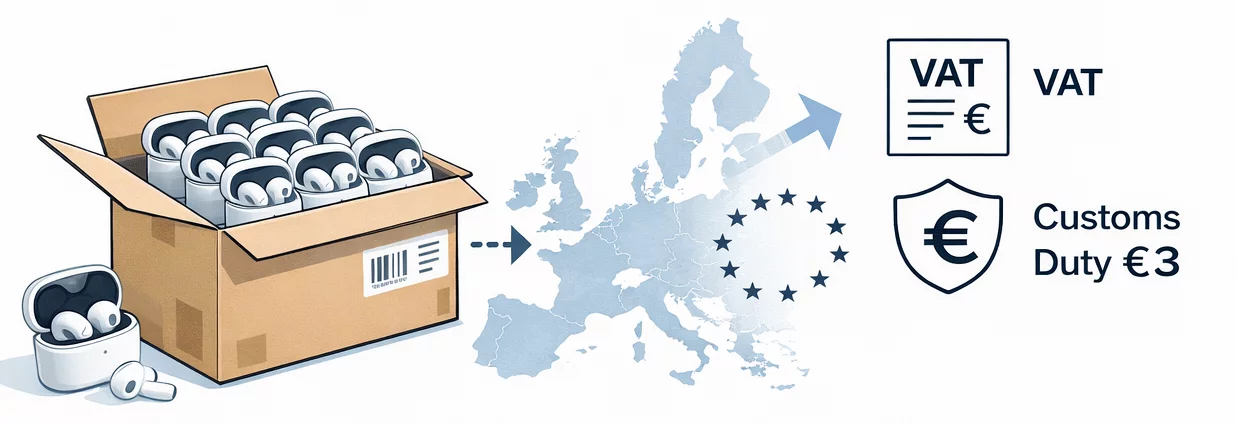

The end of 2025 brought the official confirmation of what had been discussed for some time: the EU is ending customs exemption for parcels worth below EUR 150 sent from non-EU countries to consumers in the EU. As a consequence, the existing rule, under which low-value goods sold to EU consumers have historically benefited from an exemption from customs duties, is abolished. Nonetheless, VAT still applied under mechanisms such as the Import One-Stop Shop (IOSS).

Moreover, EU policymakers agreed to introduce new interim and, eventually, permanent customs duty rules that will reshape how overseas vendors calculate costs and compliance obligations when selling into the EU Single Market. From the EU's perspective, these changes reflect broader goals of fairness, competitiveness, and administrative modernization.

Key Customs Relief for Low-Value Goods Change at a Glance

The key change centers around the removal of the EUR 150 customs duty exemption threshold for low-value consignments. To understand how this change affects overseas vendors, it is crucial to clarify how the previously established system worked. Under the existing regime, parcels below this threshold enter the EU duty-free, even though VAT and formal declarations may still apply.

What was designed as a mechanism to reduce the administrative burden of clearing millions of small shipments, which, to some extent, it did, created distortions in competition, encouraged undervaluation of goods, and complicated the enforcement of product safety and compliance rules. And the numbers prove this.

In 2024, nearly 4.6 billion low-value parcels entered the EU market, a 100% increase from 2023 and three times the 2022 total. From another perspective, almost 12 million parcels per day entered the EU in 2024, with 91% of e-commerce shipments coming from China.

In response to this trend, the European Commission proposed removing the 150 EUR customs duty relief threshold in 2023, as part of the much-awaited EU customs reform. After years of debate, in December 2025, the Council of the European Union agreed that, from July 1, 2026, a flat EUR 3 customs duty per item will be charged on goods valued at EUR 150 or less entering the EU from third countries.

The New System: What Replaces the Relief

With the final decision to remove the exemption, the EU moves forward with its reform of the customs regime and procedures. The first, interim or transitional, part of the reform is this new regime, with a fixed customs duty of EUR 3 per item, which will apply from mid-2026.

What is essential to understand is that this charge does not vary in value, nor simply per parcel or per shipment, but by item type, as classified under customs tariff headings. Consequently, consignment with multiple items could incur multiple EUR 3 fees, effectively increasing the duty bill on multi-item parcels.

Nonetheless, the EUR 3 per item fee should not be mistaken for the potential handling fee, which is a separate charge under discussion intended to cover the administrative and compliance costs associated with inspecting and processing low-value goods. Currently, the Commission is considering introducing a EUR 2 parcel fee per package.

Regarding customs fees, overseas sellers and marketplaces should expect to incorporate them into their pricing and logistics planning. However, in the long term, the EU’s Customs Data Hub and broader reforms, which will begin in 2028, will enable the calculation of duties based on existing tariff schedules and product classifications.

Note: Data in the image is from the European Commission - EU Customs Reform article

Overall Effects of Changes in EU Customs Rules

Generally, the abolishment of the EUR 150 threshold for low-value goods imported from outside the EU means that customs duties will apply from the very first euro, ending the preferential treatment these shipments previously enjoyed. As a result, importers will no longer benefit from simplified customs clearance procedures.

Additionally, the change in rules is expected to restore a level playing field between EU-based retailers and non-EU online vendors by removing a structural cost advantage that favoured cross-border e-commerce. Also, the EU regulators hope to see a decrease in the volume of low-value goods imports.

However, this raises a critical question: how does this policy change affect overseas vendors and non-EU sellers?

What This Means in Practice for Overseas Vendors

Once new customs rules come into effect, overseas vendors, non-EU sellers, and marketplaces will face several operational and commercial challenges. The first and most apparent effect is the direct impact on product pricing and competitiveness. E-commerce vendors accustomed to offering goods at prices that assumed duty-free entry into the EU may find their offers less competitive once the EUR 3 fee per item and eventual tariffs are factored into end prices.

The EUR 3 duty applies to goods sold by non-EU sellers registered with the IOSS for VAT, which covers approximately 93% of e-commerce shipments to the EU. Non-registered IOSS vendors and sellers, on the other hand, may face slower customs clearance and additional administrative costs, further incentivizing them to participate in IOSS.

Notably, the fixed duties application per item may disproportionately affect sellers of multi-item or bundled products, where each item could attract the EUR 3 duty. All of the changes could negatively affect small vendors with thin margins, who may find the cumulative impact of duties, VAT, handling fees, and compliance costs a substantial barrier to bear.

Understanding the New Calculation Metric

In addition to administrative challenges, the most notable implication of the reform is the emergence of a new calculation metric for determining customs duty and related charges. While the replaced system treated low-value parcels as duty-free up to EUR 150, the shift to a per-item fixed duty introduces a different logic, where duties are no longer tied directly to value below the threshold but rather to the presence and categorization of items in the shipment.

Example 1: Single-item parcel under EUR 150

A vendor ships a single smartwatch valued at EUR 120 to an EU customer. Under the old rules, the shipment is subject only to VAT, not to customs duty. Under the new regulations, a customs duty of EUR 3 applies in addition to VAT.

Example 2: Multi-item parcel under EUR 150

A seller ships a parcel containing three phone accessories, each valued at EUR 40, for a total of EUR 120. Under the old rules, the entire package is exempt from customs duties, whereas VAT applies. Under the new regulations, a EUR 3 duty per item category applies, resulting in an additional EUR 9 customs duty, plus VAT.

Example 3: Shipment consisting of several identical low-value products

A seller ships a parcel containing 10 identical earbuds, each valued at EUR 10, for a total of EUR 100. Previously, this parcel would be duty-free, but VAT would apply. Under the new rules, since earbuds fall under the same tariff heading, the whole parcel, not each individual earbud, is subject to a customs duty of EUR 3.

Key Takeaways

What is essential for overseas and non-EU businesses to understand is that, under the new EU rules, customs duty is calculated per item type, as classified under customs tariff headings, not on the parcel's total value. This fundamentally changes cost modeling for bundled products, multi-item orders, and high-volume shipments, making it essential for overseas vendors and sellers to update pricing, logistics, and compliance systems.

Source: VATabout - EU Ends EUR 150 Customs Threshold to Curb Undervaluation, VATabout - EU to Introduce EUR 3 Duty on Low-Value E-Commerce Parcels, VATabout - 2025 ECOFIN Report Insights: EU VAT, IOSS, and Digital Rules, European Parliament, European Commission

%22%20fill%3D%22%23FFFFFF%22%3E%3Cpath%20d%3D%22M267.109551%2C33.9224%20L301.032051%2C0%20L334.954551%2C33.9224%20L329.125351%2C39.7516%20L301.032051%2C11.6583%20L272.938751%2C39.7516%20L267.109551%2C33.9224%20Z%20M322.483751%2C64.3549%20L338.106051%2C79.9772%20L332.276951%2C85.8064%20L316.654651%2C70.1841%20L301.032051%2C85.8064%20L267.109551%2C51.8839%20L272.938751%2C46.055%20L301.032051%2C74.1483%20L329.125351%2C46.055%20L334.954551%2C51.8839%20L322.483751%2C64.3549%20Z%22%20id%3D%22Fill-3%22%3E%3C%2Fpath%3E%3Cg%20id%3D%22v%22%20transform%3D%22translate(0%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpolygon%20id%3D%22Path%22%20points%3D%2223.1661333%200%2029.9750083%200%2018.1392686%2027.7674434%2011.8357397%2027.7674434%200%200%206.99505518%200%2015.0539971%2020.2404448%22%3E%3C%2Fpolygon%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(30.6833%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(65.3066%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22a%22%20transform%3D%22translate(86.731%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M23.4055078%2C0.664929199%20L29.5228564%2C0.664929199%20L29.5228564%2C28.4323726%20L23.4055078%2C28.4323726%20L23.4055078%2C24.4427974%20C20.9585684%2C27.5458003%2017.7137139%2C29.0973018%2013.6709443%2C29.0973018%20C11.0998848%2C29.0973018%208.76819971%2C28.4634026%206.67588916%2C27.1956042%20C4.58357861%2C25.9278059%202.94785278%2C24.1856914%201.76871167%2C21.9692607%20C0.589570557%2C19.7528301%200%2C17.2792935%200%2C14.5486509%20C0%2C11.8180083%200.589570557%2C9.34447168%201.76871167%2C7.12804102%20C2.94785278%2C4.91161035%204.58357861%2C3.16949585%206.67588916%2C1.90169751%20C8.76819971%2C0.63389917%2011.0998848%2C0%2013.6709443%2C0%20C17.7314453%2C0%2020.9762998%2C1.54263574%2023.4055078%2C4.62790723%20L23.4055078%2C0.664929199%20Z%20M14.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.403146%2C5.87797412%2010.3507312%2C6.70691919%208.71057251%2C8.36480933%20C7.07041382%2C10.0226995%206.25033447%2C12.08398%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07041382%2C19.0480051%208.71057251%2C20.7058953%20C10.3507312%2C22.3637854%2012.403146%2C23.1927305%2014.8678169%2C23.1927305%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22b%22%20transform%3D%22translate(123.2691%2C%2021.9462)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M15.9051064%2C10.7984502%20C18.4584346%2C10.7984502%2020.7812539%2C11.4323494%2022.8735645%2C12.7001477%20C24.965875%2C13.967946%2026.6060337%2C15.7144934%2027.7940405%2C17.9397898%20C28.9820474%2C20.1650862%2029.5760508%2C22.6341899%2029.5760508%2C25.3471011%20C29.5760508%2C28.0600122%2028.9820474%2C30.529116%2027.7940405%2C32.7544124%20C26.6060337%2C34.9797087%2024.965875%2C36.7262561%2022.8735645%2C37.9940544%20C20.7812539%2C39.2618528%2018.4584346%2C39.895752%2015.9051064%2C39.895752%20C13.8837217%2C39.895752%2012.0396514%2C39.4879287%2010.3728955%2C38.6722822%20C8.70613965%2C37.8566357%207.28762402%2C36.6952261%206.11734863%2C35.1880532%20L6.11734863%2C39.2308228%20L-5.68434189e-14%2C39.2308228%20L-5.68434189e-14%2C0%20L6.11734863%2C0%20L6.11734863%2C15.4795518%20C7.26989258%2C13.9901104%208.68397534%2C12.8375664%2010.3595969%2C12.0219199%20C12.0352185%2C11.2062734%2013.8837217%2C10.7984502%2015.9051064%2C10.7984502%20Z%20M8.56428809%2C31.517644%20C10.2133125%2C33.1666685%2012.2612944%2C33.9911807%2014.7082339%2C33.9911807%20C17.1551733%2C33.9911807%2019.1942896%2C33.1622356%2020.8255825%2C31.5043455%20C22.4568755%2C29.8464553%2023.272522%2C27.7940405%2023.272522%2C25.3471011%20C23.272522%2C22.9001616%2022.4568755%2C20.843314%2020.8255825%2C19.1765581%20C19.1942896%2C17.5098022%2017.1551733%2C16.6764243%2014.7082339%2C16.6764243%20C12.2612944%2C16.6764243%2010.2177454%2C17.5098022%208.57758667%2C19.1765581%20C6.93742798%2C20.843314%206.11734863%2C22.9001616%206.11734863%2C25.3471011%20C6.11734863%2C27.7940405%206.93299512%2C29.8508882%208.56428809%2C31.517644%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22o%22%20transform%3D%22translate(156.5624%2C%2032.7447)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M14.8678169%2C29.0973018%20C10.6300015%2C29.0973018%207.09257812%2C27.7053833%204.25554687%2C24.9215464%20C1.41851562%2C22.1377095%200%2C18.6800776%200%2C14.5486509%20C0%2C10.4172241%201.41851562%2C6.95959229%204.25554687%2C4.17575537%20C7.09257812%2C1.39191846%2010.6300015%2C0%2014.8678169%2C0%20C17.6339224%2C0%2020.1562205%2C0.63389917%2022.4347112%2C1.90169751%20C24.7132019%2C3.16949585%2026.499645%2C4.91604321%2027.7940405%2C7.1413396%20C29.088436%2C9.36663599%2029.7356338%2C11.8357397%2029.7356338%2C14.5486509%20C29.7356338%2C17.261562%2029.088436%2C19.7306658%2027.7940405%2C21.9559622%20C26.499645%2C24.1812585%2024.7132019%2C25.9278059%2022.4347112%2C27.1956042%20C20.1562205%2C28.4634026%2017.6339224%2C29.0973018%2014.8678169%2C29.0973018%20Z%20M8.72387109%2C20.7191938%20C10.3728955%2C22.3682183%2012.4208774%2C23.1927305%2014.8678169%2C23.1927305%20C17.3147563%2C23.1927305%2019.3494397%2C22.3637854%2020.9718669%2C20.7058953%20C22.5942942%2C19.0480051%2023.4055078%2C16.9955903%2023.4055078%2C14.5486509%20C23.4055078%2C12.08398%2022.5942942%2C10.0226995%2020.9718669%2C8.36480933%20C19.3494397%2C6.70691919%2017.3147563%2C5.87797412%2014.8678169%2C5.87797412%20C12.4208774%2C5.87797412%2010.3728955%2C6.71135205%208.72387109%2C8.37810791%20C7.07484668%2C10.0448638%206.25033447%2C12.1017114%206.25033447%2C14.5486509%20C6.25033447%2C16.9955903%207.07484668%2C19.052438%208.72387109%2C20.7191938%20Z%22%20id%3D%22Shape%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22u%22%20transform%3D%22translate(191.1474%2C%2033.4096)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M12.8464321%2C28.4323726%20C8.98097705%2C28.4323726%205.87354126%2C27.3596201%203.52412476%2C25.2141152%20C1.17470825%2C23.0686104%200%2C20.2315791%200%2C16.7030215%20L0%2C0%20L6.09075146%2C0%20L6.09075146%2C15.9051064%20C6.09075146%2C17.8910283%206.71135205%2C19.4912913%207.95255322%2C20.7058953%20C9.19375439%2C21.9204993%2010.8250474%2C22.5278013%2012.8464321%2C22.5278013%20C14.8678169%2C22.5278013%2016.4902441%2C21.9249321%2017.7137139%2C20.7191938%20C18.9371836%2C19.5134556%2019.5489185%2C17.9087598%2019.5489185%2C15.9051064%20L19.5489185%2C0%20L25.6396699%2C0%20L25.6396699%2C16.7030215%20C25.6396699%2C20.2315791%2024.4693945%2C23.0686104%2022.1288437%2C25.2141152%20C19.788293%2C27.3596201%2016.6941558%2C28.4323726%2012.8464321%2C28.4323726%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3Cg%20id%3D%22t%22%20transform%3D%22translate(221.2498%2C%2026.2018)%22%20fill-rule%3D%22nonzero%22%3E%3Cpath%20d%3D%22M18.6446147%2C12.7400435%20L10.7984502%2C12.7400435%20L10.7984502%2C25.8790444%20C10.7984502%2C27.1557085%2011.1486462%2C28.1176394%2011.8490383%2C28.7648372%20C12.5494304%2C29.4120349%2013.5468242%2C29.7356338%2014.8412197%2C29.7356338%20C16.0646895%2C29.7356338%2017.3324878%2C29.4164678%2018.6446147%2C28.7781357%20L18.6446147%2C34.4965269%20C17.1374419%2C35.258979%2015.4440889%2C35.6402051%2013.5645557%2C35.6402051%20C10.6388672%2C35.6402051%208.43130225%2C34.8688872%206.94186084%2C33.3262515%20C5.45241943%2C31.7836157%204.70769873%2C29.6292451%204.70769873%2C26.8631396%20L4.70769873%2C12.7400435%20L0%2C12.7400435%20L0%2C7.20783252%20L4.70769873%2C7.20783252%20L4.70769873%2C0%20L10.7984502%2C0%20L10.7984502%2C7.20783252%20L18.6446147%2C7.20783252%20L18.6446147%2C12.7400435%20Z%22%20id%3D%22Path%22%3E%3C%2Fpath%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fg%3E%3C%2Fsvg%3E)